%2520PayRam.png&w=3840&q=75)

February 19, 2025

Ask GPT about this BlogHow Crypto Payments & Stablecoins Unlock Cross-Border Commerce (2025 Strategy)

I. The Global Payments Friction Index: Measuring Legacy Failure Points

The reliance on outdated traditional payment systems actively erodes merchant profitability through high fees, costly chargebacks, and unacceptable cross-border latency.

I.1. The Erosion of Profit: Quantifying Credit Card and Wire Transfer Drag

Legacy transaction costs, exemplified by a standard 3% credit card fee, silently divert critical funds away from business growth and expose merchants to billions in annual fraud risk.

Traditional payment systems stifle growth. Credit cards, bank transfers, and legacy processors aren’t just outdated they actively work against your bottom line. That “industry-standard” 3% credit card fee quietly erodes approximately $30,000 annually from a business generating $1 million in revenue. This is before hidden costs like chargeback fees, PCI compliance audits (Payment Card Industry Data Security Standard), and the immense systemic exposure to fraudulent disputes, estimated to cost merchants collectively around $40 billion yearly. This massive financial leakage limits internal capacity for expansion. Consequently, businesses must seek transparent, low-cost alternatives offered by a modern crypto payments processor. The elimination of the chargeback mechanism inherent in crypto transactions, discussed further in our deep dive on eliminating the chargeback mechanism, represents an absolute defense against this colossal form of digital commerce fraud.

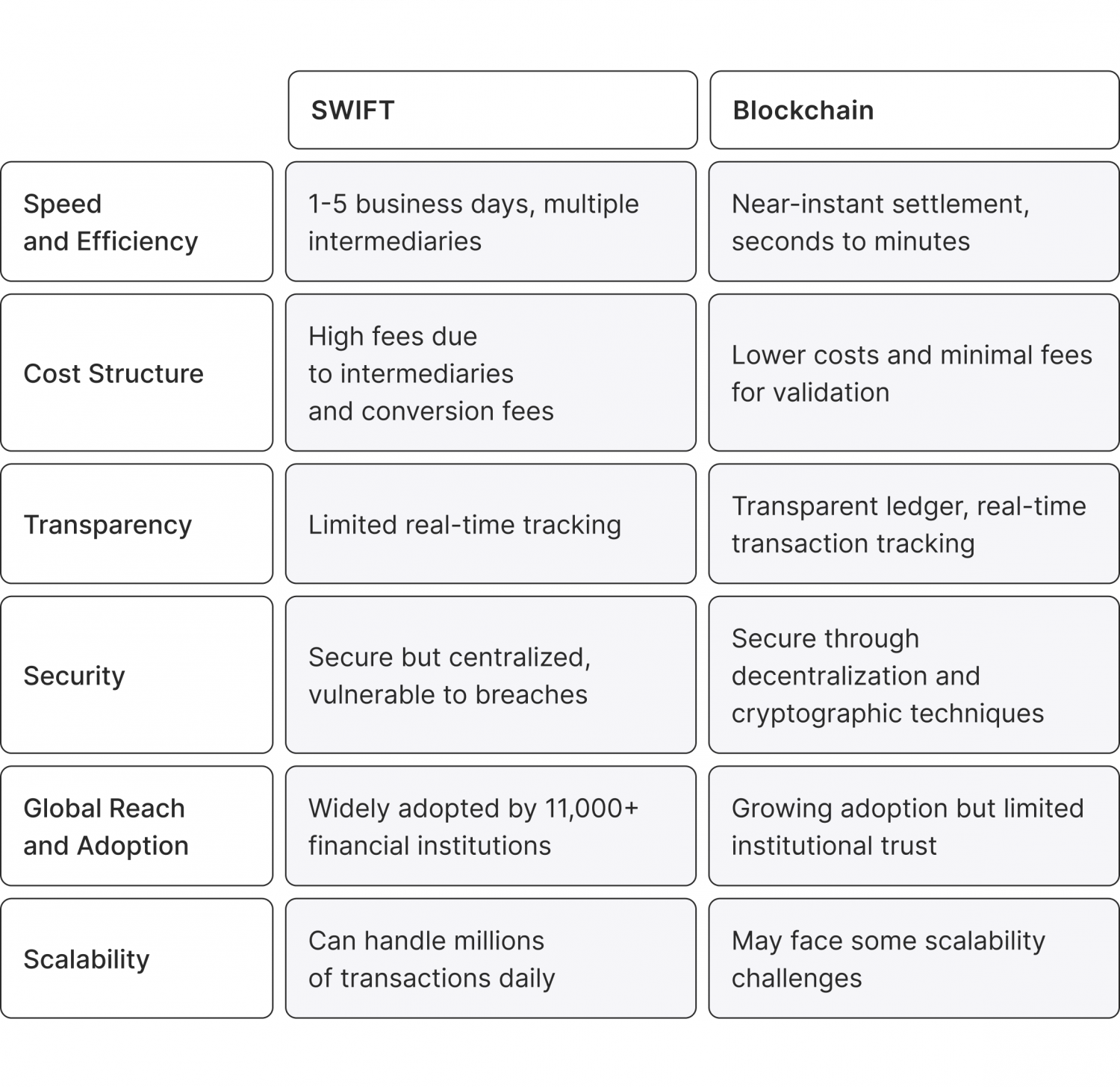

I.2. Time vs. Speed: Analyzing Cross-Border Latency (SWIFT vs. Blockchain)

While antiquated SWIFT networks impose days-long delays and friction, decentralized blockchain infrastructure offers instantaneous, 24/7 global settlement, fulfilling urgent market demand for accelerated value transfer.

“Instant” bank transfers often mean 3-5 business days of waiting—a lifetime in today’s fast-paced e-commerce world. While your cash flow stalls, customers grow impatient, and competitors gain ground. Cross-border transactions relying on outdated networks like SWIFT (Society for Worldwide Interbank Financial Telecommunication) perpetuate friction and significant latency. By contrast, crypto-forward businesses settle payments in minutes, 24/7.

For example, a Shopify store in Berlin can receive payment from a São Paulo customer via Ethereum in 90 seconds. Market demand for these faster rails is intense, evidenced by high interest in solutions like cross border payments solutions and cross border payments blockchain , highlighting the commercial demand for accelerated, decentralized payment rails.

Industry Statistic: Traditional cross-border payments often cost between 2% to 7% of the transaction value when accounting for transfer fees, FX spreads, and intermediary charges.

Hélène Rey, Professor at the London Business School, assesses that widespread stablecoin adoption unlocks the positive side of "faster and cheaper cross-border payments".

II. The Emerging Market Imperative: Financial Inclusion as a Growth Vector

Financial inclusion driven by crypto is a critical commercial strategy that unlocks billions in untapped revenue potential by serving populations ignored by traditional banking.

II.1. The Unbanked Thesis: Digital Wallets as the New Banking Infrastructure

Crypto provides essential financial access to the 1.3 billion people still unbanked by leveraging widely accessible smartphones and wallets, bypassing traditional barriers like credit checks and documentation.

Traditional banks and card networks act as gatekeepers, severely limiting access. While global financial inclusion efforts have made progress, reducing the unbanked population from 2.5 billion in 2011 to roughly 1.3 billion by 2025, a massive commercial opportunity remains. Access only necessitates a smartphone, a globally ubiquitous technology, owned by an estimated 5.3 billion people, and a crypto wallet application such as MetaMask or Trust Wallet. This direct-to-digital model has already accelerated inclusion efforts, contributing to the narrowing of the global financial gender gap in account ownership from 7.4% in 2017 to 4.4% in 2021.

II.2. Crisis-Driven Adoption: Case Studies in High-Inflation Economies

In high-inflation economies like Argentina and Turkey, stablecoins become essential economic tools for citizens seeking stability and accessible commerce outside of volatile local fiat currencies.

In countries like Turkey, Argentina, and Nigeria, local currencies face severe devaluation and instability. This economic climate has propelled many consumers to seek alternatives, transforming cryptocurrencies from a speculative asset into a tool for economic survival. Hyperinflation, for example, has made traditional savings nearly impossible in Argentina. Citizens and merchants turn to stablecoins like USD Coin (USDC) or Tether (USDT) which function as reliable "digital dollars" to transact and preserve wealth, mitigating the volatility risks inherent in local monetary systems.

II.3. LatAm and Southeast Asia: Demographics and Digital Readiness

Youthful, digitally native populations in markets like Vietnam and the Philippines are poised for crypto adoption, creating a high-growth sector best served by leveraging efficient stablecoin cross border payments.

The young and tech-savvy populations in Vietnam and the Philippines represent another goldmine for digital merchants. With low credit card penetration and a high reliance on remittances, these markets are ripe for disruption. Cryptocurrencies provide a cheaper and faster alternative to traditional money transfer services. By utilizing stablecoins (USDT/USDC), businesses can cater to these demographics with payment options that prioritize stability and speed, making stablecoin cross border payments a clear strategic focus for market entry. Learn more about how crypto payments enable global trade.

Industry Statistic: The cross-border payments market is racing toward $290 trillion by 2030, driven largely by the efficiency of blockchain and stablecoin rails.

Yao Zeng of the University of Pennsylvania Wharton School states that the widespread changes in finance mean "The global financial landscape has changed, yet the rules remain largely unchanged".

III. Cryptoeconomics and the Cost Arbitrage Strategy

By dissolving multiple intermediaries, crypto payment systems deliver predictable, ultra-low transactional costs that structurally maximize merchant profit margins.

III.1. Cost Compression Mechanics: Why Crypto Payments Win on Margin

Compared to traditional credit card fees that take 3% of revenue, the transparent, typically 1% or less pricing model of crypto payments directly yields exponential savings for merchants.

Let’s talk dollars and cents. Traditional payment systems bleed your profits with layers of fees, but crypto cuts the middlemen and the costs out of the equation. The math doesn’t lie. A $1,000 credit card sale costs you about $30 in fees. That same sale via Bitcoin is roughly $2. Over 10,000 transactions, you save $280,000—enough to fund major organizational growth initiatives. Crypto gateways charge transparent fees, typically 1% or less for advanced services. This effectively eliminates opaque "qualified vs. non-qualified" rate games and other hidden PCI compliance surcharges.

III.2. The Stabilization Solution: USD-Pegged Stablecoins (USDC and USDT) in Commerce

Stablecoins like USDC and USDT are crucial tools that mitigate cryptocurrency's volatility, bridging the gap between blockchain efficiency and the stability demands of traditional commerce, despite persistent market concerns over stablecoin security risks.

Stablecoin supply has grown from roughly $5 billion to over $305 billion as of September 2025. However, market apprehension is visible, as suggested by queries like stablecoin security risks, confirming the need for businesses to prioritize rigorously audited, highly liquid assets and employ technology that ensures instant auto-conversion. For a detailed market outlook, consult our analysis on robust stablecoin support.

III.3. Technical Efficiency: Leveraging Low-Cost, High-Speed Chains

The operational efficacy of a modern blockchain payment system depends on selecting high-throughput, low-cost networks like Tron (TRX) and Solana (SOL) to handle high volumes of low-value stablecoin transfers.

For optimal cost arbitrage—especially in high-volume e-commerce, gaming, or mass payroll—the selection of the underlying blockchain network is critical. Networks like Tron and Solana offer superior transactional throughput and minimal fees, making them highly efficient platforms for stablecoin settlements. This technological efficiency ensures the promise of a low-cost blockchain payment system is delivered consistently across global operations. You can master the economics of these networks by learning how to optimize fees when leveraging low-cost, high-speed chains.

Industry Statistic: Total global stablecoin supply surged from $5 billion to over $305 billion as of September 2025, demonstrating explosive institutional and consumer trust in digital dollars.

The adoption of these rails signifies a systemic shift, confirming that "2025 is a turning point for cross-border blockchain adoption" as solutions transition from niche applications to mass enterprise infrastructure.

IV. The High-Risk Vertical: Censorship Resistance as a Feature

For restricted industries facing arbitrary exclusion by centralized financial gatekeepers, specialized, self-hosted crypto infrastructure guarantees essential business autonomy.

IV.1. The Gatekeeper Problem: Why Traditional Processors Reject Restricted Industries

Centralized processors wield disproportionate power, resulting in account freezing or termination for high-risk merchants, a chronic pain point evident in high search volumes for terms like "stripe restricted businesses adult content policy 2025" and "stripe account closed".

Centralized payment processors wield immense discretionary authority, actively excluding high-revenue sectors such as iGaming, casinos, and adult platforms. This exclusion leads to operational risk and merchant anxiety. When centralized policy is enforced, merchants face account freezing or termination like "stripe account closed". This systemic risk mandates a move away from relying on conventional high-risk payment processors that structurally restrict business operations.

High-Risk Businesses: How to Accept Payments Without Getting Banned (2025 Survival Guide)

byu/SatansVault insmallbusiness

IV.2. Self-Hosted Autonomy: Architectural Advantages of Non-Custodial Gateways

A self-hosted crypto payment gateway provides the highest level of sovereignty, granting merchants complete, non-custodial control over their funds and the ability to forgo mandatory KYC/KYB requirements.

The self-hosted, non-custodial model offers restricted industries the highest degree of sovereignty. This means the merchant retains complete control and possession of their funds and data, ensuring censorship resistance against arbitrary bans. PayRam is deployed via Docker and features flexible compliance tools that allow for optional KYC implementation while prioritizing privacy and autonomy, a key feature of a truly sovereign, self-hosted crypto payment gateway.

IV.3. Competitive Landscape Review: Gateways for Restricted Markets

While managed custodial services offer convenience, the self-hosted non-custodial model provides the necessary censorship resistance and business continuity required by restricted verticals like iGaming.

| Criterion | PayRam | Competitor (Generic Custodial) |

|---|---|---|

| Core Model | Self-Hosted / Non-Custodial | Managed / Custodial |

| Mandatory KYC | No (Optional Compliance Tools) | Yes |

| Fiat Conversion | External Partners (On/Off-Ramps) | Instant, Internal |

| High-Risk Tolerance | High (Censorship-Resistant) | Medium (Subject to Ban) |

The global high-risk payment gateway market was valued at USD 6.5 billion in 2023 and is expected to reach about USD 15.2 billion by 2032, reflecting the massive value flowing through these verticals.

"In high-risk commerce, control over the payment gateway is not a feature but an operational necessity to guarantee business continuity against arbitrary third-party restrictions."

V. Implementation and Strategic Mandate

The transition to crypto is a strategic move that demands a measured operational playbook to capitalize on emerging demographics and secure a leading position in the future of commerce.

V.1. Operational Playbook: Integrating Crypto Payments Seamlessly

To successfully implement and scale, businesses must learn how to accept crypto payments as a business by starting small, leveraging data, and actively promoting their adoption of efficient blockchain payment solutions.

The path to crypto adoption should be deliberate and phased. Start by selecting a gateway that offers seamless integration via API or plugins for major e-commerce platforms. Initial deployment should utilize Stablecoins (USDC) on a single product line to neutralize volatility during the testing phase. Once integrated, actively promote the new rail, recognizing that crypto holders tend to be younger (43% under 35) and spend 25% more online than older cohorts. The key is knowing how to accept crypto payments as a business and scaling based on the market response to your blockchain payment solutions. This proactive promotion builds brand loyalty and attracts tech-savvy buyers, exemplified by luxury retailers reporting significant sales boosts, as discussed further in our guide on boosting customer loyalty.

V.2. Regulatory and Risk Mitigation

Crypto payments inherently mitigate transactional risk, such as chargebacks, and regulatory challenges are managed through proactive compliance tools rather than avoiding the transparent public ledger system.

Fears of regulatory backlash and criminal activity are largely outdated. Every transaction on a public blockchain is recorded in an immutable ledger, offering greater transparency and accountability than traditional financial systems. Furthermore, while global compliance standards like the FATF (Travel Rule) evolve, this is a manageable challenge for providers employing modular, proprietary compliance tools that the merchant controls. Most importantly, crypto's irreversible transactions eliminate the core vulnerability of the legacy system: the costly chargeback mechanism.

V.3. Strategic Mandate (2025-2030)

With web3 finance rapidly approaching ubiquity, the time for executive decision-making is now to either lead the market shift or risk being perpetually relegated to playing catch-up.

The cumulative data is clear: cryptocurrency payments will be as conventional as PayPal within the next five years. The shift to web3 finance is not just about efficiency it's an existential necessity for global commerce. By embracing sovereign, stablecoin-based payment infrastructure today, businesses gain instant access to high-growth emerging markets and retain significantly more of their revenue. This proactive approach cultivates a modern, forward-thinking brand image that commands customer loyalty. The path of least resistance—clinging to traditional financial systems—equates to perpetually accepting high fees, long settlement delays, and severe operational restriction imposed by centralized gatekeepers.

The global iGaming market alone is projected to reach $117.5 billion in 2025 and grow to $169.2 billion by 2030, making efficient crypto payment rails essential for capturing this enormous revenue.

This revolution is now unfolding with stablecoins operating across borders 24/7 at very low cost and signals that it is high time for global commerce to embrace the new frontiers of finance.

Frequently Asked Questions (FAQ)

1. What is the Core Financial Benefit of Using a Self-Hosted Crypto Gateway

The primary benefit is the elimination of high intermediary fees like the standard 3% credit card processing charge. PayRam’s core self-hosted transaction collection offers a self-custody structure for processing, meaning more profit margin stays with the merchant.

2. How are Chargebacks Handled with Crypto Payments

Crypto payments utilize irreversible blockchain technology. This fundamentally eliminates the risk of chargebacks and subsequent associated fees (estimated at $40 billion annually industry-wide). Once a transaction is validated, the settlement is final.

3. Does PayRam Support Fiat On-Ramp and Off-Ramp Services

Yes. While PayRam is a non-custodial crypto processor, it integrates seamlessly with specialized fiat on-ramp and Off-Ramp partners such as MoneyGram. This allows customers to convert fiat currency into crypto for payment and merchants to convert received crypto back into fiat.

4. Why is PayRam Better for High-Risk Industries than BTCPay Server

PayRam is built specifically for enterprise growth, offering robust, out-of-the-box support for stablecoins on low-fee networks like Tron, a crucial requirement for iGaming and large-scale global e-commerce that older self-hosted models often lack.

5. How do Stablecoins (USDC/USDT) Mitigate Volatility for Merchants

Stablecoins are cryptocurrencies pegged 1:1 to a stable asset like the U.S. Dollar. By enabling automatic conversion of incoming crypto payments into USDC or USDT, merchants shield their treasury from price swings, providing the stability of a digital dollar.

6. What are the Most Cost-Effective Blockchains for Enterprise Payments

For high-volume, low-value stablecoin transfers, Tron (TRX) and Solana (SOL) are the most cost-effective networks. They are favored due to their massive transaction throughput and minimal network fees.

7. What is the "Unbanked Thesis" for Global Growth

The unbanked thesis explains that by adopting crypto, businesses gain instant access to 1.3 billion adults globally who lack traditional bank accounts but own smartphones. This opens huge, untapped e-commerce revenue potential in emerging markets.

8. Does PayRam require Mandatory KYC

No. As a non-custodial, self-hosted gateway, PayRam does not impose mandatory Know Your Customer (KYC) requirements, prioritizing merchant privacy and autonomy. However, it offers optional, modular compliance tools that can be deployed autonomously.

9. How much Faster are Crypto Cross-Border Payments than Traditional Methods

Traditional SWIFT transfers can take 3-5 business days for settlement. Crypto payments, especially using stablecoins on fast networks, achieve final settlement in minutes, 24 hours a day, providing a critical competitive edge in global cash flow.

10. How Streamlined is the PayRam Setup Process

PayRam uses a streamlined UI-based setup via Docker deployment, which significantly reduces the technical complexity traditionally associated with configuring self-hosted, multi-chain crypto payment infrastructure.

Ready to seize control of your payments, eliminate legacy fees, and enter the $1.3 billion unbanked market?

Explore PayRam's self-hosted solution and documentation now