October 13, 2025

Ask GPT about this BlogThe Ultimate Guide to On-Chain Payments: A Merchant's Playbook for the Future of Commerce

In the last fiscal year, businesses lost an estimated 2-5% of their revenue to cross-border transaction fees, settlement delays, and chargeback fraud. What if you could reclaim that margin with on-chain payments, settle globally in seconds, and eliminate chargebacks entirely? This isn't a future promise. It's the current reality of blockchain technology.

For Pragmatic Tech Leaders, navigating the world of on-chain payments is a high-stakes endeavor. It promises unprecedented efficiency but is shrouded in technical complexity, security concerns, and regulatory uncertainty. This guide cuts through the noise.

We will deconstruct the entire on-chain payment ecosystem, starting with the foundational "what" and "why." We'll then provide a step-by-step playbook for implementation, compare on-chain rails to traditional finance, address the critical challenges of security and compliance, and finally, look ahead to the future of digital commerce.

Part I: The Genesis of On-Chain Commerce: Defining the New Financial Rails

"With e-currency based on cryptographic proof, without the need to trust a third party middleman, money can be secure and transactions effortless." – Satoshi Nakomoto, Developer of Bitcoin

On-chain payments are transactions recorded, verified, and settled directly on a blockchain, removing the need for traditional financial intermediaries. Unlike conventional methods that rely on a series of banks and processors, an on-chain transaction is a direct, peer-to-peer exchange of digital value. The entire lifecycle—from initiation to the moment funds are irrevocably settled in a merchant's account—is inscribed as a permanent record on a public ledger.

To grasp this model, contrast it with a credit card payment. That transaction routes through an acquiring bank, a card network like Visa, and an issuing bank. Each intermediary adds cost and delay, resulting in settlement times of several business days.

On-chain payments collapse this structure. The blockchain itself acts as the single, global network for clearing and settlement in one automated step. It's also important to distinguish these from off-chain transactions like Bitcoin's Lightning Network, which process transactions outside the main blockchain for speed and are settled on-chain later. This guide focuses on the on-chain layer as the ultimate source of truth and finality, a concept crucial for businesses in sectors like iGaming and online casinos where transaction finality is paramount.

Part II: Anatomy of an On-Chain Transaction: The Core Components

This section deconstructs the technical ecosystem into understandable components for a business leader, focusing on the practical implications of each element.

The global blockchain technology market is projected to grow from USD 31.18 billion in 2025 to USD 393.42 billion by 2032, exhibiting a staggering CAGR of 43.65%. This explosive growth underscores the rapid adoption of the underlying technology for payments and other applications.

The On-Chain Ecosystem: Wallets, Blockchains, and Smart Contracts

A successful on-chain transaction relies on the interplay between a digital wallet to hold assets, a blockchain to process the transaction, and smart contracts to automate agreements.

Digital wallets are the user interface for the blockchain, acting as a digital bank account. They come in two main types:

- Custodial Wallets: Managed by a third party like an exchange that holds your private keys. This is convenient but introduces counterparty risk.

- Non-Custodial Wallets: You hold your own private keys, granting full sovereignty over your funds. This is the most secure model for businesses but requires responsible key management. Understanding seed phrases and HD wallets is the first step toward true financial self-sovereignty.

The blockchain network functions as the payment rails. A key distinction is between Layer 1 (L1) foundational blockchains like Ethereum or Solana, and Layer 2 (L2) scaling solutions built on top of them. The high transaction fees on some L1s have driven the adoption of L2s for more commercially viable payment processing.

Finally, smart contracts provide the business logic. These are self-executing programs on the blockchain that can automate complex payment flows, such as recurring subscriptions, escrow services, or real-time revenue sharing, without requiring costly intermediary services. This is a core component of the comprehensive guide to cryptocurrency payments.

Choosing Your Rails: A Comparison of Popular Payment Blockchains

Selecting the right blockchain network involves a strategic trade-off between transaction speed, cost, security, and ecosystem maturity.

There is a tiny outside chance that crypto rails can grow fast enough and different and weird enough that they can disrupt the duopoly business models [of Apple and Google].” – Anatoly Yakovenko, Founder of Solana

The market has matured beyond a simple focus on Bitcoin (BTC). Users are now actively comparing payment-oriented blockchains like TRON (TRX) and Solana (SOL), connecting their need for low transaction fees with the specific features of these networks.

- Ethereum (ETH): The most established smart contract platform, offering unparalleled security and decentralization. Its high Layer 1 fees are offset by a vibrant Layer 2 ecosystem like Polygon that processes transactions for a fraction of the cost.

- Tron (TRX): Has gained significant traction for payments due to consistently low transaction fees and high throughput. Popular for cost-effective stablecoin transfers.

- Solana (SOL): Built for speed, boasting extremely high throughput and sub-cent transaction fees. Growing recognition as a high-performance payment rail for use cases like point-of-sale systems.

| Network | Average Transaction Fee | Average Transaction Speed (Time to Finality) | Primary Use Case for Payments | Ecosystem Maturity |

|---|---|---|---|---|

| Ethereum (Layer 1) | $2 - $20+ (variable) | ~13 minutes | High-value settlement, DeFi backbone | Very High |

| Solana | <$0.001 | ~2.5 seconds | Point-of-sale, high-frequency payments, micropayments | High |

| TRON | <$0.01 (often near-zero with energy) | ~3 minutes | Stablecoin transfers, low-cost B2C/P2P payments | High |

| Polygon (L2 on Ethereum) | <$0.01 | ~2-5 minutes (with checkpoints to L1) | E-commerce, gaming, general-purpose payments | Very High |

Part III: Taming Volatility: The Critical Role of Stablecoins in Commerce

This section tackles the single biggest obstacle to mainstream adoption for commerce: price volatility. The transaction volume for stablecoins surged to $5.7 trillion in 2024 and accelerated with a 66% spike in Q1 2025, according to a report by Flagship advisory partners. This highlights their central role in the on-chain economy.

Why Volatility is a Non-Starter for Business (And How Stablecoins Fix It)

Stablecoins are cryptocurrencies pegged to a real-world asset like the U.S. dollar, eliminating the price volatility that makes native cryptocurrencies impractical for commerce.

Native cryptocurrencies like Bitcoin or Ether can fluctuate dramatically in minutes, introducing an unacceptable level of risk into routine business operations. If a merchant accepts 0.05 ETH for a $150 product and the price of ETH drops 10% before they can convert to fiat, they have lost 10% of their revenue. This risk makes financial planning and accounting nearly impossible.

Stablecoins solve this. By maintaining a 1:1 peg, they provide the benefits of on-chain payments—speed, low cost, and global reach—without the volatility. Learn more about stablecoin. Stablecoins enable predictable revenue streams, simplify treasury management, and allow businesses to operate within the digital asset economy while denominating their operations in a familiar, stable unit of account. This is a key reason why stablecoin payments are reshaping global commerce.

A Taxonomy of Stability: Fiat-Collateralized, Crypto-Collateralized, and Algorithmic

Stablecoins achieve their price peg through different mechanisms, with fiat-collateralized coins being the most trusted for commercial transactions.

“A stablecoin is essentially a cryptocurrency designed to maintain a stable value relative to a certain asset... The market cap of the basket of stablecoins we track ended June +2% higher month over month, sustaining seven consecutive months of positive market cap growth.” – Kenneth Worthington, J.P. Morgan Analyst

- Fiat-Collateralized Stablecoins: For every stablecoin issued, an equivalent amount of fiat currency is held in reserve in audited bank accounts. Issuers like Circle (for USDC) and Tether (USDT) provide regular attestations to verify their backing. This model provides a high degree of trust, which is why these assets dominate the on-chain payments landscape.

- Crypto-Collateralized Stablecoins: These are backed by a surplus of other cryptocurrencies held in smart contracts. This model is more decentralized but also more complex and carries risk during extreme market volatility.

- Algorithmic Stablecoins: This model uses algorithms to manage the token's supply to maintain its price peg. terra usd serves as a powerful reminder of the significant risks associated with this model, as evidenced by its collapse. For business purposes, fiat-collateralized stablecoins are the clear and prudent choice.

Part IV: A Merchant's Playbook: How to Accept On-Chain Payments

This is the strategic heart of the guide, providing actionable, comparative pathways for implementation. The number of U.S. consumers using crypto for payments is projected to grow by 82% between 2024 and 2026, according to research firm Emarketer, signaling a massive shift in consumer behavior that merchants must prepare for.

Choosing Your Integration Path: Three Models for Accepting On-Chain Payments

Businesses can accept on-chain payments directly to a wallet, through a third-party gateway, or via a self-hosted gateway, a choice that impacts cost, complexity, and control. Choosing your integration path is a critical strategic decision that will impact your transaction costs, operational complexity, and customer experience.

Key Questions for Your Evaluation

Before choosing a path, a pragmatic tech leader should frame their thinking with these questions:

- What level of technical resources can I dedicate to this project?

- How critical are censorship resistance and full custody of funds to my business model?

- What is my transaction volume, and how sensitive is my margin to processing fees?

- What kind of checkout experience does my customer expect?

Method 1: The Direct-to-Wallet Approach (For Freelancers and Small Businesses)

The simplest method involves providing customers with a public wallet address, offering low complexity but requiring manual tracking and management.

The process is straightforward: a business creates a non-custodial wallet and shares the public address (or a QR code) with the customer. The primary advantages are simplicity and zero intermediary fees. However, this approach requires manual reconciliation of every transaction and offers a disjointed user experience for e-commerce, making it difficult to scale.

Method 2: Third-Party Payment Gateways (The Plug-and-Play Solution)

Custodial payment gateways like BitPay or Coinbase Commerce handle the entire payment process, from checkout to fiat conversion, in exchange for a transaction fee.

These crypto payment processors provide APIs and plugins for popular e-commerce platforms like Shopify and WooCommerce. They offer a seamless customer experience and can automatically convert crypto receipts into fiat currency deposited into a business's bank account. The convenience is significant, but it comes at the cost of a processing fee (typically ~1%) and custodial risk, as the gateway takes temporary control of the funds and can be a point of censorship. This is a key differentiator in the Payram vs Coinbase Commerce debate.

Method 3: The Self-Hosted Gateway (The Sovereignty Solution)

A self-hosted payment gateway like PayRam is open-source software that runs on your own server, providing a non-custodial, self-custody processing solution that offers complete control.

"I don't understand why anyone would not accept crypto for payments. It is easier, faster and cheaper to integrate than traditional payment gateways. Less paperwork. And reaches a more diverse demographic and geography." – Changpeng Zhao, Founder & CEO of Binance

Instead of relying on a third party, a business deploys the software on its own server. Payments go directly from the customer's wallet to the business's wallet, with no intermediary. Users are actively seeking self hosted crypto payment processors to avoid fees and custodial risk. For businesses that prioritize sovereignty, especially those in high-risk industries like adult entertainment or iGaming, a self-hosted, enterprise-grade solution is the superior choice.

The advantages are compelling:

- self-custody: With PayRam, there's no processor in the middle. The only costs are blockchain network fees ("gas") and server maintenance. Advanced services like payment orchestration are optional add-ons with commercial terms discussed privately; the core gateway is self-hosted, so no third-party processor takes a cut of your payments.

- Full Custody: The business always maintains control of its private keys. This "no keys on server" architecture is your only true defense against deplatforming.

- Censorship Resistance: No third party can freeze accounts or block transactions, a vital feature for merchants who have had issues where Stripe closed their account.

- Enhanced Privacy & Easy Setup: Transaction data is not shared with a third party. With PayRam, setup is streamlined through a simple UI, eliminating complex command-line configurations.

| Integration Model | Ideal For | Setup Complexity | Transaction Fees | Custody Model | Fiat Conversion | Scalability |

|---|---|---|---|---|---|---|

| Direct-to-Wallet | Freelancers, small businesses, donations | Low | Network fees only | Non-Custodial (Full Control) | Manual | Low |

| Third-Party Gateway | E-commerce, retail, businesses seeking convenience | Low | ~1% + network fees | Custodial (Third-Party) | Automatic | High |

| Self-Hosted Gateway (PayRam) | Tech-savvy businesses, high-volume merchants, privacy-focused orgs | Low (UI-Based) | Self-hosted; network fees only | Non-Custodial (Full Control) | Manual or via OffRamp Service | Very High |

For a detailed breakdown, see our (https://payram.com/blog/payram-vs-btcpay-server-which-self-hosted-gateway-is-right-for-you).

Part V: A Comparative Framework: On-Chain vs. Traditional Financial Rails

This section provides a direct, evidence-based comparison to help the persona build a business case for adopting on-chain payments.

"In traditional finance, the main pillar of the system is that you have to trust the company you're doing business with... You don't have full control of your money. The source of trust is public governance, financial authorities, laws, licenses... In short, the trust is put in people, not code and math." – Computools Analysis on Traditional Finance

The Business Case: On-Chain Payments by the Numbers

On-chain payments offer quantifiable advantages over traditional finance in transaction costs, settlement speed, and global accessibility.

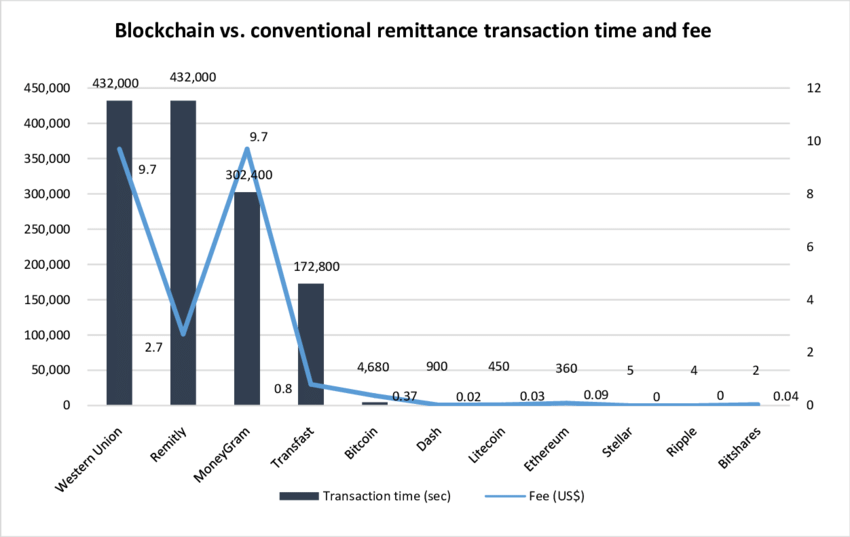

- Transaction Fees: Traditional credit card payments typically incur fees of 2.9% + $0.30. On-chain payments on efficient networks can cost fractions of a cent, representing pure margin that drops directly to the bottom line.

- Settlement Speed: Traditional finance operates on a T+2 or T+3 basis. On-chain transactions are settled with the finality of the blockchain, ranging from a few seconds on networks like Solana to around 13 minutes on Ethereum, dramatically improving liquidity.

- Global Accessibility: On-chain payments are inherently borderless. A single wallet address is all a business needs to accept payments from anyone, anywhere in the world, 24/7, bypassing the slow and expensive correspondent banking system for international payments. This is key for reaching new markets.

Perhaps the most profound shift is the elimination of chargebacks. Blockchain transactions are immutable and cannot be reversed. This concept of finality presents both a major advantage and a new responsibility. For merchants, this effectively allows them to permanently eliminate fraudulent chargebacks. However, it also means businesses must implement clear internal processes for handling legitimate customer refunds, as there is no third-party arbiter.

Part VI: Navigating the Gauntlet: Security, Compliance, and Risk Mitigation

This section addresses the advanced concerns of a prudent business leader, focusing on practical strategies for securing assets and navigating the regulatory landscape.

Compelling Statistic: In 2024, hackers stole $2.2 billion in cryptocurrency, with DeFi platforms being the top targets. This highlights the absolute necessity of robust, self-custodied security protocols for any business operating on-chain.

Fortifying Your Treasury: Advanced Security Protocols

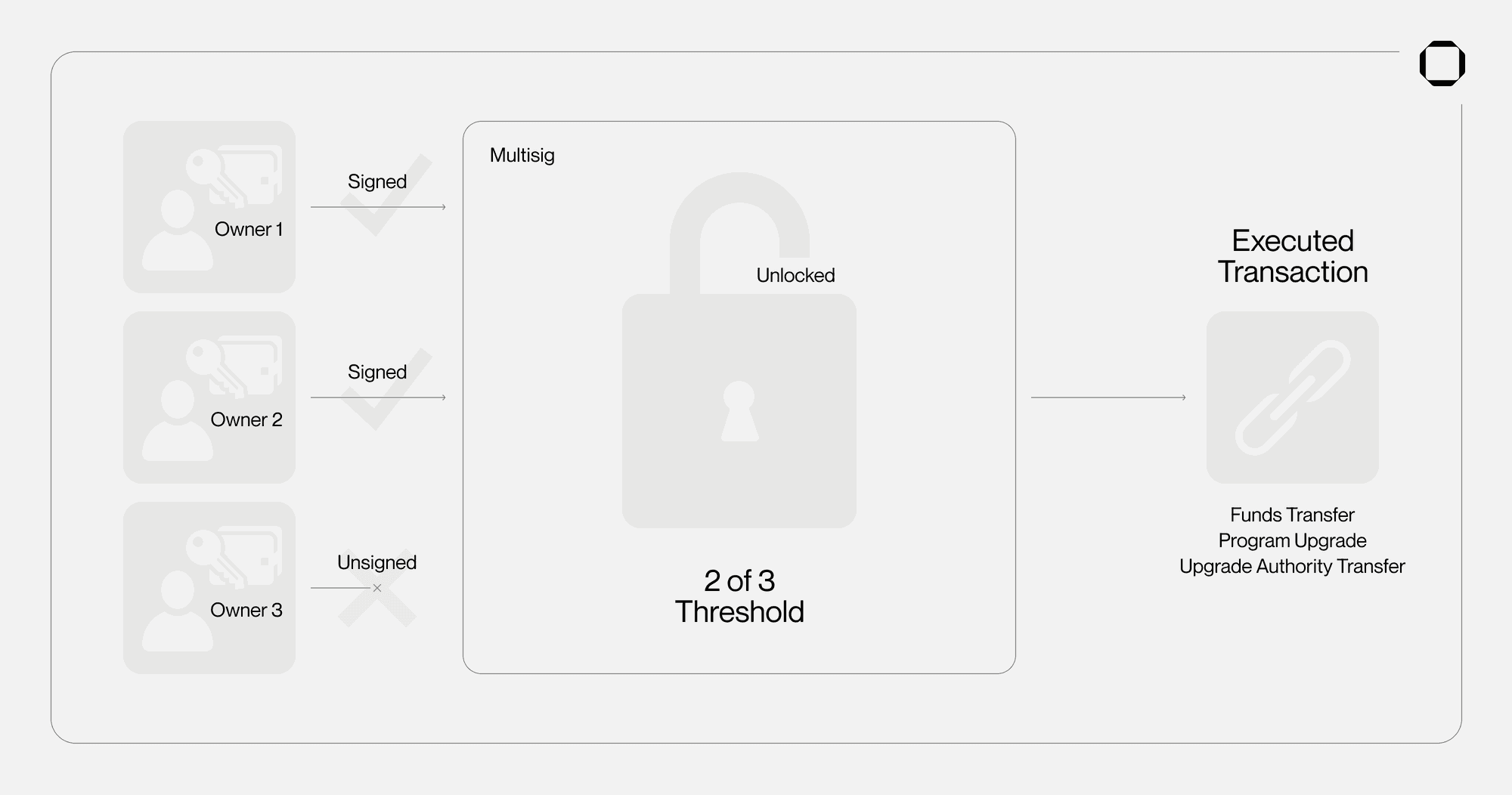

Securing business funds in an on-chain environment requires robust operational security, including the use of hardware wallets and multi-signature configurations.

"Multisig wallets give you the security you need to hold assets with peace of mind... Not only do multisig wallets protect your funds if you lose a key, but they also keep your assets protected if an attacker manages to compromise one of your keys through a hack or theft." – Casa, on Multisig Wallets

The industry standard for securing significant corporate funds is the multi-signature (multi-sig) wallet. This wallet requires more than one private key to authorize a transaction (e.g., 2-of-3 keys held by the CEO, CFO, and CTO). This architecture protects against external theft, insider threats, and the accidental loss of a single key. For maximum security, these keys should be stored on hardware wallets like Ledger or Trezor, which keep them in an offline "cold storage" environment. This is the foundation of building your crypto fortress.

The Compliance Tightrope: Traceability, Privacy, and KYC

Navigating the balance between user privacy and regulatory requirements like Know Your Customer (KYC) and Anti-Money Laundering (AML) is a critical compliance challenge.

Contrary to the myth of total anonymity, most on-chain transactions are publicly traceable. This traceability creates a tension between user privacy, valued by those searching for crypto payments without kyc, and regulatory compliance, a necessity for businesses in regulated industries. For businesses that must comply, third-party gateways often have built-in KYC checks. For those using a self-hosted solution like PayRam, integrating with a blockchain intelligence provider like chainalysis is essential for analyzing the source of funds and meeting reporting obligations like the FATF (Travel Rule).

Part VII: The Horizon: Future Trends Shaping On-Chain Payments

This final section provides forward-looking analysis, positioning the reader ahead of the curve. A base case estimate from Citigroup projects that stablecoin issuance will reach $1.9 trillion by 2030, supporting nearly $100 trillion in annual transaction activity.

The Future of On-Chain Commerce: What's Next for Digital Payments?

The evolution of on-chain payments will be defined by increasing regulatory clarity, the emergence of Central Bank Digital Currencies (CBDCs), and deeper integration with the programmable economy of Web3.

"In an environment of geoeconomic transformations... the on-chain economy is emerging as the protagonist of a new era. More than an isolated trend, this economy connects technological advances with fundamental monetary changes." – Drew Anderson, VanEck, via Bit2Me News

Comprehensive regulatory frameworks like the 2025 EU’s MiCA (Markets in Crypto-Assets) are providing the legal certainty enterprises need to adopt on-chain payments. The rise of Central Bank Digital Currencies (CBDCs) will also shape the landscape, likely coexisting with private-sector stablecoins.

Looking further ahead, the true power of on-chain payments will be unlocked through deeper integration with the programmable economy of Web3. The ability to embed payment logic directly into smart contracts opens up a vast design space for new business models like real-time revenue sharing and automated royalty payments. Understanding the fundamentals of on-chain payments, stablecoins, and self-custody is the essential first step for any business looking to thrive in this coming decade of financial innovation.

Conclusion

The transition to on-chain payments represents a fundamental shift in the architecture of commerce. The core benefits are clear: a drastic reduction in transaction costs, near-instant global settlement, and the complete elimination of chargeback fraud. By leveraging stablecoins, merchants can access these advantages without exposure to asset volatility.

The path to implementation varies, from simple Direct-to-Wallet methods to convenient third-party gateways and sovereign self-hosted solutions like PayRam. Each path requires a deliberate approach to security and an awareness of the evolving compliance landscape. On-chain payments are no longer a niche experiment. They are a strategic tool available today that offers a significant competitive advantage for any forward-thinking business.

Frequently Asked Questions (FAQ)

1. What is the main advantage of on-chain payments over credit cards?

The primary advantages are drastically lower fees, near-instant settlement times (seconds vs. days), and the elimination of fraudulent chargebacks. While credit cards charge merchants around 2-3%, on-chain transactions can cost less than a cent on efficient networks.

2. Are on-chain payments anonymous?

No, they are pseudonymous. While your real-world identity isn't directly attached to your wallet address, all transactions are recorded on a public, permanent ledger. This traceability is a key feature for compliance and security.

3. Do I need to be a crypto expert to accept on-chain payments?

Not necessarily. While direct-to-wallet methods require some knowledge, third-party gateways offer a plug-and-play experience similar to traditional processors. PayRam goes a step further for self-hosting, providing a streamlined UI-based setup to simplify what was once a highly technical process.

4. How do businesses handle the price volatility of cryptocurrencies?

By using stablecoins. These are digital currencies pegged 1:1 to a stable asset like the U.S. dollar (e.g., USDC, USDT). This allows businesses to get all the benefits of blockchain rails without being exposed to the price swings of assets like Bitcoin or Ethereum.

5. What is the difference between a custodial and a non-custodial wallet?

With a custodial wallet, a third party (like an exchange) holds your private keys and controls your funds. With a non-custodial wallet, you hold your own keys, giving you complete control and sovereignty over your assets. Self-hosted gateways like PayRam are non-custodial by design.

6. Can a crypto payment be reversed like a credit card chargeback?

No. On-chain transactions are final and immutable once confirmed on the blockchain. This is a major benefit for merchants as it eliminates chargeback fraud. However, it means businesses must have their own clear policies for handling legitimate customer refunds.

7. What is a "self-hosted" payment gateway?

A self-hosted gateway is software you run on your own server. This makes you your own payment processor, cutting out intermediaries. It provides maximum control, censorship resistance, and cost savings, as you only pay for network fees and server costs, not percentage-based processing fees.

8. What are OnRamp and OffRamp services?

OnRamp services allow users to easily convert traditional fiat currency (like USD) into cryptocurrency. Off-Ramp services do the reverse, allowing businesses to convert their crypto receipts back into fiat currency in their bank accounts. PayRam offers these services to bridge the gap between the traditional and on-chain financial worlds.

9. Is it difficult to set up a self-hosted gateway like PayRam?

Historically, it required significant technical expertise. However, PayRam was designed with a streamlined, UI-based setup process, making it accessible to a broader range of tech-savvy business leaders without needing deep command-line knowledge.

10. Which blockchain is best for payments?

It depends on your needs. Ethereum offers unmatched security for high-value transactions. TRON is extremely popular for low-cost stablecoin transfers. Solana offers near-instant speed for high-volume applications like retail or gaming. PayRam supports multiple chains, allowing you to choose the best rail for each transaction.

Take Control of Your Financial Destiny

Stop letting traditional payment processors dictate your margins, hold your cash flow hostage, and threaten your business with deplatforming. The future of commerce is direct, decentralized, and in your control.