November 28, 2025

Ask GPT about this BlogThe Protocol Wars: ACP vs. AP2 vs. TAP—and the Missing Link in the Agentic Economy

The Buy button—a fixture of the internet for twenty-five years—is becoming obsolete. We are witnessing the end of Human-to-Business (H2B) commerce and the rise of Agent-to-Business (A2B) commerce. In this new paradigm, the primary economic actors are not humans navigating visual interfaces, but autonomous AI agents executing complex, multi-step workflows based on logic and intent.

This is not a future prediction; it is a current reality. Daily queries for purchasable products on platforms like ChatGPT have already surged to approximately 53 million, representing a massive shift in how value is discovered and exchanged. However, agentic commerce faces a critical infrastructure crisis. Legacy payment rails, designed for human latency, manual fraud checks, and visual CAPTCHAs, are fundamentally incompatible with the millisecond speed and deterministic needs of AI agents. To fill this vacuum, tech giants are racing to define the rules of the road with three competing yet complementary standards: ACP, AP2, and TAP.

"The agentic economy—commerce facilitated or executed by autonomous software—could account for between $3 trillion and $5 trillion in global transaction volume by 2030." — McKinsey & Company

While these protocols solve the problems of permission and identity, they leave a gaping hole regarding settlement. This is where the true battle for the agentic economy will be fought—and where PayRam provides the critical Execution Layer.

The Buy Button is Dying: Welcome to the Agentic Web

The friction between the high-speed, logic-driven world of AI agents and the slow, manual, permission-gated world of traditional finance has created a crisis of infrastructure. Agents do not browse visually; they ingest structured data via APIs. They do not trust based on aesthetics, they verify cryptographic signatures. Most critically, they cannot pay efficiently using infrastructure designed for legacy card settlements which are plagued by high fees and slow finality.

This shift necessitates a move toward programmatic payments that match the speed of software. The market is reacting with three dominant frameworks, each championing a different layer of the transaction lifecycle: Application, Governance, and Identity.

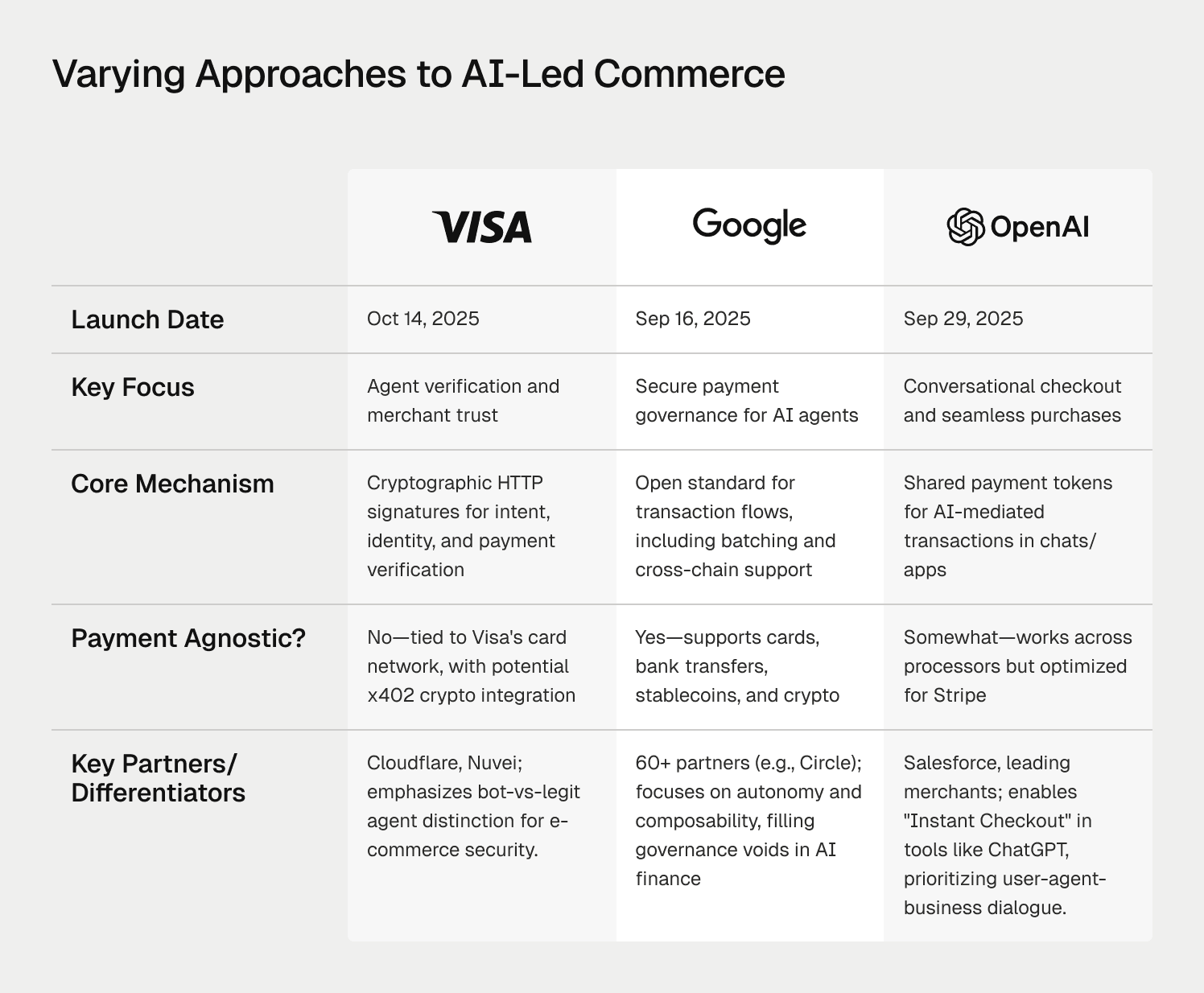

The Landscape Defined: The Big Three Protocols

The emerging agentic stack is currently defined by three dominant frameworks from the titans of Silicon Valley and the financial establishment.

What is the Agentic Commerce Protocol (ACP)?

ACP is an open standard co-developed by OpenAI and Stripe that functions as a tactical bridge, enabling AI agents to initiate purchases directly within conversational interfaces like ChatGPT using existing payment rails.

Spearheaded by OpenAI and Stripe, the Agentic Commerce Protocol (ACP) focuses on immediate utility and user experience. It is designed to be the Application Layer that makes instant checkout possible within LLMs. Its core innovation is the Shared Payment Token (SPT). Instead of exposing sensitive raw card data to an AI agent, ACP generates a scoped, bounded, and ephemeral token that the agent passes to the merchant. Crucially, ACP allows the merchant to remain the Merchant of Record, handling liability and fulfillment while the AI simply facilitates the intent.

What is Google's Agent Payments Protocol (AP2)?

AP2 is Google's infrastructure-layer protocol designed to solve the complex "Principal-Agent" problem through a system of cryptographically signed "Mandates" that provide a non-repudiable audit trail for every agent action.

While ACP solves for speed, Google's Agent Payments Protocol (AP2) solves for governance. Backed by a coalition of over 60 partners, AP2 is built for complex, high-stakes environments. It introduces Mandates—verifiable digital credentials (VCs)—that cryptographically bind a user's intent to an agent's action. An Intent Mandate proves the user asked for a purchase, a Cart Mandate locks in the merchant's offer, and a Payment Mandate executes the trade. This structure makes AP2 payment-rail agnostic, capable of carrying instructions for credit cards, bank transfers, or even stablecoin payments via extensions.

"AP2 is designed to ensure that as AI agents begin to shop and pay on behalf of users, transactions remain secure, auditable, and accountable across the payments ecosystem." — Google Cloud & PayPal Announcement

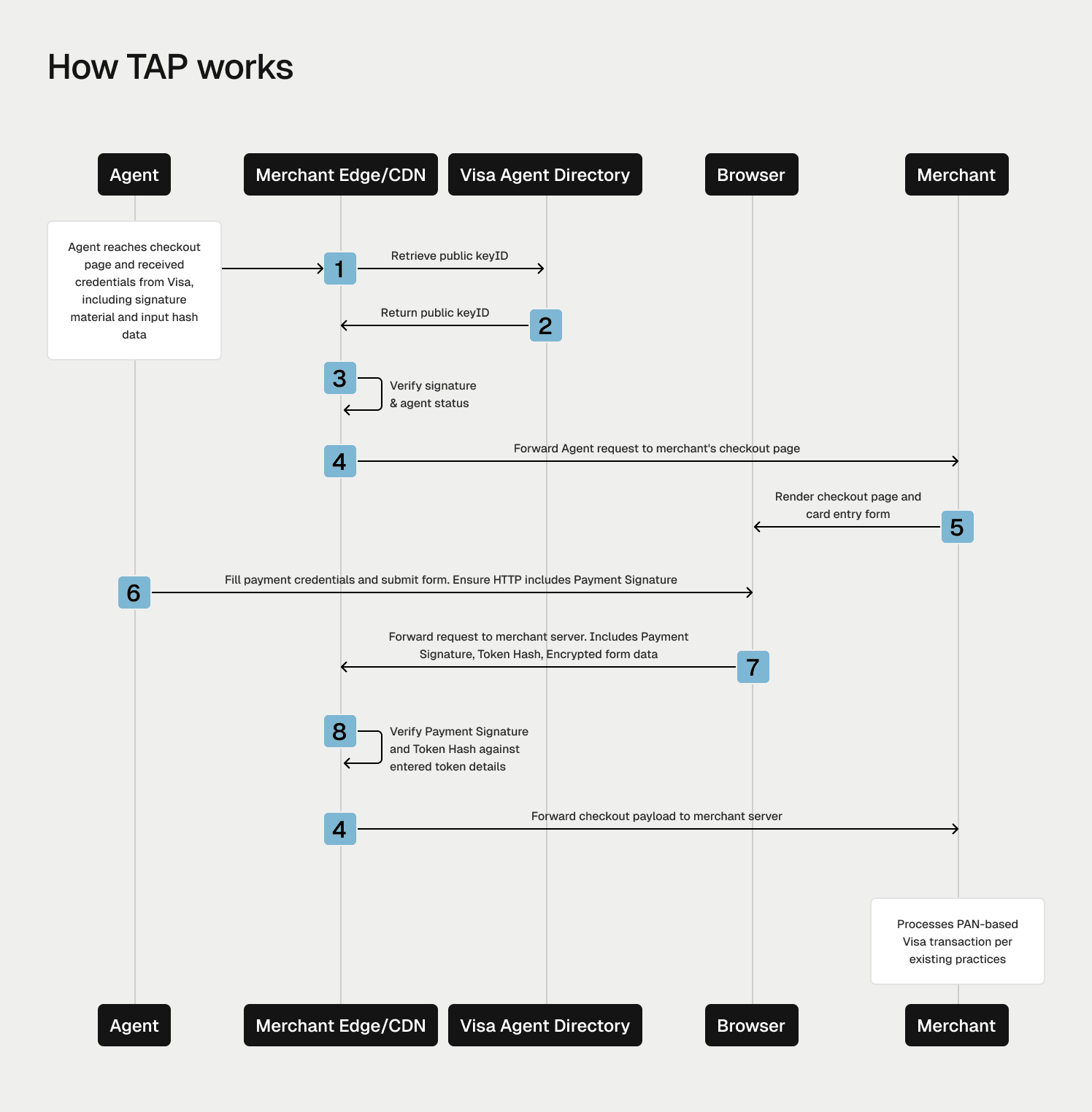

What is Visa's Trusted Agent Protocol (TAP)?

TAP is an identity-layer framework developed by Visa and Cloudflare that uses Public Key Infrastructure (PKI) to distinguish legitimate, high-intent AI shopping agents from malicious bots and scrapers.

Merchants today are under siege from bad bots, leading many to block automated traffic entirely. Visa's Trusted Agent Protocol (TAP) acts as the Digital Passport to reopen these doors. It enables agents to sign their HTTP requests with a private key, which merchants (or edge networks like Cloudflare) can verify against Visa's registry. Beyond simple access, TAP allows agents to securely pass user context—such as loyalty IDs or shipping preferences—without a full login, solving the cold start problem for guest checkouts.

Critical Comparison: ACP vs. AP2 vs. TAP

Understanding the agentic economy requires viewing these standards not merely as competitors, but as distinct layers in a nascent technology stack that manages different aspects of trust and execution.

What is the difference between ACP and AP2?

ACP is optimized for immediate, conversational retail experiences using legacy card rails, while AP2 provides a robust, rail-agnostic governance framework for complex, autonomous workflows.

| Feature | OpenAI ACP | Google AP2 | Visa TAP |

|---|---|---|---|

| Primary Function | Application Layer: UX & Instant Checkout | Governance Layer: Permission & Audit | Identity Layer: Bot Verification |

| Core Mechanism | Shared Payment Tokens (SPTs) | Cryptographic Mandates (VCs) | Digital Signatures (PKI) |

| Philosophy | "Tactical Bridge" (Works now with Stripe) | "Structural Foundation" (Long-term infrastructure) | "Digital Passport" (Gatekeeper for bots) |

| Settlement Rail | Defaults to Cards (Fiat) | Rail-Agnostic (Cards, RTP, Crypto) | N/A (Identity Only) |

| Ideal Use Case | Retail/B2C (Buying shoes in ChatGPT) | Enterprise/B2B (Procurement, Complex Workflows) | Security/Anti-Fraud (Allowing good bots) |

While ACP is winning the race for consumer mindshare via ChatGPT, AP2 is building the plumbing for a broader agentic commerce ecosystem.

The Protocol Stack: How They Work Together

Rather than mutually exclusive standards, ACP, AP2, and TAP are likely to form a Corporate Stack where TAP handles identity, AP2 manages authorization, and ACP executes the interface interaction.

In a mature agentic transaction, these protocols will interoperate. Imagine an agent buying travel tickets:

- Identity (TAP): The agent presents its Visa TAP signature to bypass the airline's bot firewall.

- Governance (AP2): The agent presents a signed AP2 Mandate proving the user authorized a spend of up to $500 for flights to London.

- Application (ACP): The agent uses the ACP API to select the seat and pass the payment token.

However, even this sophisticated stack hits a wall at the final step: the actual movement of funds.

The Execution Gap: Why Protocols Aren't Enough

Despite the sophistication of AP2's mandates and TAP's identity verification, the entire Corporate Stack relies on legacy banking rails that are too slow, expensive, and reversible for a true machine economy.

The Elephant in the Room: Legacy Banking Rails

Traditional payment systems utilize T+2 settlement times and high transaction fees, creating friction that negates the efficiency gains of autonomous AI agents. The Big Three protocols are largely wrappers around the credit card networks of the 1970s. This introduces critical bottlenecks for AI agents:

- Latency: Agents operate in milliseconds, but banks settle in days. This traps liquidity and prevents real-time supply chain optimization.

- Fees: Fixed costs (e.g., $0.30 + 2.9%) make micro-transactions impossible. An agent cannot pay $0.05 for a single API call or data packet using a credit card.

- Liability: The risk of friendly fraud and chargebacks remains high. If an agent hallucinates a purchase, the merchant is often left liable.

"Visa saw a 25% increase in malicious bot-initiated transactions over the past 6 months... a share expected to grow as agentic commerce scales." — Visa Security Report

Why AI Agents Need PayFi and Stablecoins

PayFi (Payment Finance) applies decentralized finance mechanics to real-world payments, offering programmable, instant settlement that matches the Time Value of Money (TVM) requirements of autonomous software.

Agents operate on logic and code; they require money that behaves the same way. This is the promise of PayFi and stablecoins. Unlike fiat, which moves via messages between siloed ledgers, stablecoins like Tether (USDT) or USDC move as bearer assets on a unified ledger. This enables instant finality (no chargebacks), programmability (smart contracts), and streaming payments (paying by the second). For the agentic economy to scale beyond simple retail into complex machine-to-machine (M2M) value exchange, it needs a crypto-native settlement rail.

PayRam: The Sovereign Execution Layer

PayRam bridges the gap between the compliant governance of the corporate protocols and the speed of the crypto economy, providing the necessary "Execution Layer" for autonomous agents.

How PayRam Solves the Settlement Bottleneck

PayRam offers a non-custodial, crypto-native gateway that enables instant, final settlement for agentic transactions, eliminating chargeback risk and enabling permissionless commerce. PayRam is not a competitor to AP2 or ACP, it is the Sovereign Execution Layer that powers them.

- Zero Chargebacks: Crypto transactions are irreversible. Once an agent pays, the deal is final. This is crucial for high-risk merchants or high-velocity agent markets.

- Instant Settlement: Funds arrive in the merchant's wallet in seconds, not days, maximizing capital efficiency.

- Permissionless Access: Unlike Stripe or PayPal, which can de-platform agents for arbitrary reasons, PayRam's non-custodial architecture ensures that commerce remains open and censorship-resistant.

Implementing the Mullet Economy (AP2 + PayRam)

The Mullet Economy strategy combines the business in the front compliance of AP2 Mandates with the party in the back efficiency of PayRam's stablecoin rails.

This hybrid approach offers the best of both worlds. An enterprise can use Google AP2 to generate the necessary compliance and audit trails (Intent and Cart Mandates) to satisfy regulators and internal policy. However, when it comes time to execute the Payment Mandate, the agent routes the transaction through PayRam using stablecoins. This ensures that the transaction is fully compliant and authorized (Web2) but settles instantly and cheaply (Web3).

Native Web3 Commerce with x402 and ERC-8004

PayRam natively integrates with emerging Web3 standards like x402 (Payment Required) and ERC-8004 Protocol (Trustless Agents) to facilitate truly autonomous, machine-to-machine commerce.

- x402: PayRam listens for the revived HTTP 402 Payment Required status code. When an agent hits a PayRam-enabled endpoint, it receives a challenge (price and address) and pays instantly to unlock the resource—perfect for pay-per-inference or data access.

- ERC-8004: PayRam fills the Trust Gap in the ERC-8004 standard. While ERC-8004 registers an agent's identity on-chain, PayRam provides the escrow logic to hold funds until the agent cryptographically proves it has completed its task, enabling trustless collaboration between strangers.

Conclusion: Preparing for the Machine Economy

The Protocol Wars are defining the traffic lights of the new economy—who can go, where they can go, and how they identify themselves. But PayRam is building the pavement.

To succeed in the Agentic Web, businesses cannot rely solely on the permission layers of ACP, AP2, or TAP. They must also control the Execution Layer. By integrating PayRam, you equip your infrastructure with the speed, finality, and sovereignty required to service the trillions of dollars in volume that autonomous agents will soon command.

Don't let legacy rails throttle your autonomous future. Equip your agents with the Sovereign Execution Layer.

Frequently Asked Questions (FAQ)

What is the difference between Agentic Commerce Protocol (ACP) and Agent Payments Protocol (AP2)?

ACP (by OpenAI/Stripe) is an application-layer protocol focused on enabling instant checkout within chat interfaces like ChatGPT. It prioritizes speed and UX. AP2 (by Google) is a governance-layer protocol that uses cryptographic mandates to create an audit trail for agent actions, solving the principal-agent problem. AP2 is better suited for complex B2B or high-value workflows.

Does PayRam work with Google AP2?

Yes. AP2 is a carrier protocol, meaning it can carry instructions for various payment methods. PayRam fits into the AP2 framework as a stablecoin settlement rail. An agent can present an AP2 mandate that authorizes a specific payment, which is then executed via PayRam's infrastructure using USDC or USDT for instant settlement.

How does Visa's Trusted Agent Protocol (TAP) prevent bot fraud?

TAP uses Public Key Infrastructure (PKI). Legitimate AI agents sign their web requests with a digital private key. Merchants (or edge networks like Cloudflare) verify this signature against Visa's registry. If the signature is valid, the bot is allowed through, if not, it is blocked. This helps merchants distinguish shopping bots from scraping bots.

Why are stablecoins better for AI agents than credit cards?

Credit cards have high fixed fees (~$0.30) and slow settlement (T+2 days). AI agents often need to make micro-payments (e.g., $0.05 for data) or transact 24/7 with instant finality. Stablecoins on high-speed chains (like Solana or Tron) allow agents to send value as easily as sending an email, with fractions of a cent in fees.

What is the x402 protocol?

x402 stands for Payment Required, a revived HTTP status code. It is a standard for machine-to-machine payments where a server responds to a request with a price and a crypto address. The agent pays instantly to unlock the resource. PayRam provides the infrastructure for merchants to easily accept x402 payments.

Can I use PayRam for high-risk industries like iGaming?

Yes. PayRam is specifically architected for high-risk merchants in industries like iGaming and Adult. Its non-custodial nature means you are not subject to the arbitrary de-platforming risks common with providers like Stripe or PayPal.

What is PayFi and how does it relate to agents?

PayFi (Payment Finance) is the use of DeFi mechanics for real-world payments. For agents, PayFi enables things like streaming payments (paying for compute power by the second) and programmable escrow (releasing funds only when a task is verified), which are impossible with traditional banking.

How does PayRam handle chargebacks?

PayRam eliminates them. Crypto transactions are irreversible. Once an agent sends funds, the settlement is final. This solves the Friendly Fraud issue where users might claim their AI agent went rogue to get a refund. For valid disputes, PayRam supports refund capabilities, but the control remains with the merchant.

Do I need to be a crypto expert to integrate PayRam?

No. PayRam provides simple API documentation and pre-built widgets. You can integrate stablecoin acceptance into your agentic workflow with just a few lines of code, similar to integrating Stripe.

Is PayRam custodial or non-custodial?

PayRam is non-custodial. We do not hold your funds. Payments go directly from the agent's wallet to your self-hosted wallet. This ensures you have 100% sovereignty over your revenue and eliminates counterparty risk.