November 07, 2025

Ask GPT about this BlogPayFi vs. DeFi: A Strategic Framework for Choosing Your Financial Stack

Beyond the Buzzword: The Evolution from Open Finance to Optimized Payments

This section traces the evolution of blockchain finance from Bitcoin's initial concept to the specialized emergence of PayFi as a necessary layer between traditional finance and DeFi.

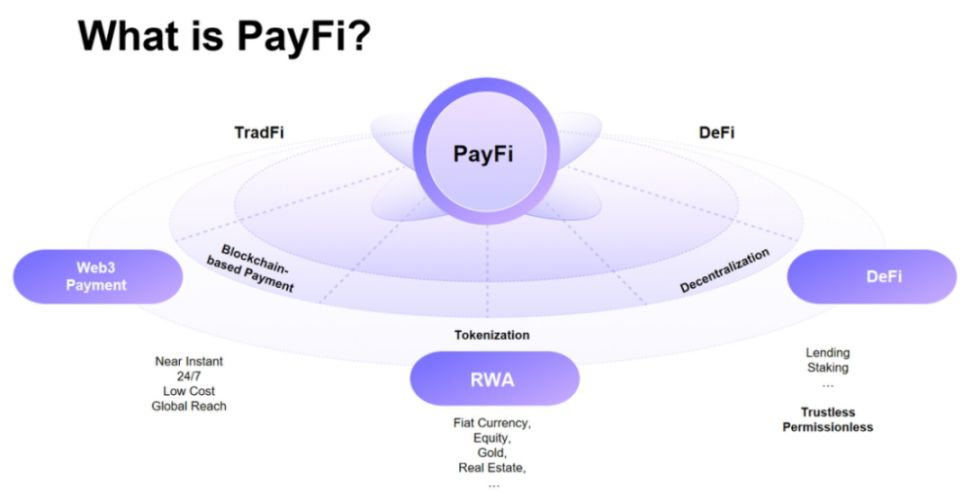

The journey of blockchain finance is one of constant evolution, starting with Bitcoin's foundational vision and quickly branching into new paradigms. The first major shift, Decentralized Finance (DeFi), unleashed a universe of open financial instruments. However, as the industry matures, a more focused and pragmatic evolution is taking shape: Payment Finance (PayFi). What is PayFi? - best understood as a critical convergence layer, bridging the gap between the legacy systems of Traditional Finance (TradFi) and the innovative but often impractical world of DeFi. This distinction is crucial, framing the core thesis of the modern financial stack: DeFi's primary goal is making "parked capital" productive, whereas PayFi’s singular mission is optimizing "money in motion".

The emergence of PayFi is a direct market response to DeFi's inherent limitations in serving the massive global payments market, which McKinsey estimates generated $2.2 trillion in revenue in 2023 alone.

As Cuy Sheffield, Head of Crypto at Visa, noted, "We think that stablecoins and CBDCs will coexist... the big opportunity for us is to continue to be that network of networks."

This highlights the need for a solution focused purely on efficient value transfer, a gap that PayFi is perfectly positioned to fill.

What is Decentralized Finance (DeFi)? A Foundational Refresher

This section defines Decentralized Finance (DeFi) as a permissionless ecosystem of financial applications built on public blockchains that use smart contracts to eliminate intermediaries.

Decentralized Finance, or DeFi, represents a global, open alternative to the current financial system. It is an ecosystem of financial applications built on public, permissionless blockchains like Ethereum. The core mission of DeFi is to disintermediate traditional finance by replacing trusted third parties with automated, self-executing smart contracts. This architecture is built on several key principles: decentralization, composability ("money legos"), and open access. The entire ecosystem, which is detailed in this comprehensive guide to cryptocurrency payments, has grown exponentially, with the Total Value Locked (TVL) in DeFi protocols reaching over $100 billion as of late 2025, according to data from DeFi Llama.

How Does DeFi Work?

DeFi operates through decentralized applications (DApps) that allow users to interact with automated smart contracts on a blockchain, managing their assets directly via crypto wallets.

At its core, DeFi works by allowing users to interact with financial protocols through decentralized applications (DApps) built on blockchains like Ethereum. Instead of relying on a bank, users connect their personal crypto wallets to these DApps, giving them full and direct control over their assets. These interactions are governed by smart contracts, which automatically execute transactions when specific conditions are met.

Foundational components like liquidity pools and automated market makers (AMMs) enable many of DeFi's functions, allowing for peer-to-peer trading and lending without a central order book.

Top Use Cases of DeFi

The primary applications of DeFi include decentralized lending and borrowing, peer-to-peer trading on DEXs, yield farming, and the creation of stablecoins and synthetic assets.

DeFi's innovative structure has given rise to a host of crypto-native financial activities. The most prominent use cases include:

- Lending and Borrowing: Platforms like Aave and Compound allow users to lend their crypto assets to earn interest or borrow against their holdings in a collateralized, peer-to-peer fashion.

- Decentralized Exchanges (DEXs): Protocols such as Uniswap facilitate the direct, peer-to-peer trading of digital assets from users' wallets, using automated market makers instead of traditional intermediaries.

- Yield Farming and Staking: Users can provide liquidity to DeFi protocols or lock up their assets to help secure a network, earning rewards in the form of interest, fees, or additional tokens.

- Stablecoins: DeFi has spurred the creation of crypto-collateralized or algorithmic stablecoins, like DAI.

- Synthetic Assets & Derivatives: DeFi enables the creation of on-chain tokens that track the value of other assets—both crypto and real-world—without requiring custody of the underlying asset.

Why DeFi Falls Short for Mainstream Payments

DeFi is ill-suited for mainstream payments due to significant challenges with high transaction costs, complex user experience, and persistent regulatory ambiguity.

Despite its innovations, pure DeFi has struggled to gain traction in the mainstream payments sector. This is due to several fundamental limitations that make it impractical for high-volume, low-value commercial transactions:

- Scalability and Cost: High transaction ("gas") fees and network congestion on blockchains like Ethereum can make small, frequent payments impractical.

- User Experience (UX) Friction: The DeFi user journey is notoriously complex. It requires a significant level of technical understanding to manage wallets, private keys, and interact with contracts, creating a formidable barrier to entry for the average user.

- Regulatory and Compliance Ambiguity: The permissionless nature makes implementing mandatory KYC/AML procedures difficult, hindering enterprise adoption. The evolving landscape, including Europe's 2025 MiCA revolution, aims to address this, but pure DeFi protocols remain in a gray area.

The Emergence of PayFi: A New Layer for Programmable Payments

PayFi has emerged as a specialized financial layer for programmable payments, a concept popularized by Lily Liu of the Solana Foundation to address the shortcomings of both TradFi and DeFi.

In response to the limitations of both traditional finance and pure DeFi, Payment Finance (PayFi) has emerged as a specialized convergence layer designed specifically for the payments vertical. The concept was notably popularized by Lily Liu, President of the Solana Foundation, who framed its necessity through a core economic principle. As she stated, "PayFi is about unlocking the time value of money. Capital that is stuck in transit is capital that can't be put to work." This highlights PayFi's mission to make money move with maximum efficiency, especially when considering that the average cost to send a cross-border remittance was 6.2% in the first quarter of 2025, according to the World Bank. This new layer is built on the foundation of programmatic payments, creating a purpose-built architecture for a new financial era.

What is PayFi in Crypto?

In crypto, PayFi is a hybrid financial architecture that uses blockchain technology and stablecoins to facilitate instant, programmable, and compliant value transfers, bridging traditional and decentralized systems.

PayFi, short for Payment Finance, is a hybrid financial architecture that integrates traditional payment systems with decentralized finance protocols to enable real-time, programmable, and compliant value transfer. It leverages the core benefits of blockchain technology—speed, transparency, and low cost—and applies them specifically to the massive global payments industry. By primarily using assets with stable value, such as stablecoins (USDC, USDT), PayFi acts as a bridge, combining the reliability and compliance of traditional finance with the efficiency and automation of DeFi.

The Core Principle: Unlocking the Time Value of Money (TVM)

PayFi's fundamental principle is to unlock the Time Value of Money (TVM) by eliminating settlement delays that tie up trillions of dollars in capital, thereby increasing capital efficiency.

The central argument for PayFi is rooted in the economic principle of the Time Value of Money (TVM). This principle states that capital available now is worth more than the same amount in the future. In the traditional financial system, trillions of dollars are often locked in slow, inefficient settlement systems. PayFi's primary objective is to unlock this trapped value by enabling instant, global, and low-cost settlement, allowing capital to be deployed productively the moment it is received.

The 4 Defining Properties of a PayFi System

A true PayFi system is characterized by four key properties: deterministic value via stablecoins, near-instant settlement on high-performance blockchains, programmability through smart contracts, and a compliance-first design.

Unlike the broad nature of DeFi, a true PayFi system is defined by a set of distinct properties that collectively address the shortcomings of previous financial paradigms:

- Deterministic Value: Overwhelming reliance on assets like Tether (USDT) or other tokenized real-world assets (RWAs) to eliminate price volatility.

- Instant or Near-Instant Settlement: Built on high-performance blockchains like Solana, Stellar, or L2s to reduce settlement from days to seconds.

- Programmability: Use of smart contracts for automated payment logic like payroll streaming, revenue splitting, and conditional payments.

- Compliance-First Design: Integration of identity verification (KYC/AML) at the protocol or application layer, a crucial feature for navigating compliance in self-hosted processors.

PayFi vs. DeFi: A Head-to-Head Comparison

This section provides a direct comparison of PayFi and DeFi, highlighting their fundamental differences in architecture, economic models, and strategic priorities.

While both PayFi and DeFi leverage blockchain and smart contracts, their architectural philosophies and business models are fundamentally different.

Bank for International Settlements (BIS) states, "While the 'DeFi' label is often applied loosely, a common thread is the aim to automate, decentralise and reconfigure financial services."

PayFi takes this automation and applies it with a singular focus on payments, creating a distinct value proposition. This is especially true for high-risk merchant survival, where the choice of infrastructure has immediate business consequences.

Architecture & Priorities: Throughput vs. Composability

DeFi's architecture prioritizes open composability, allowing protocols to be combined like "money legos," whereas PayFi's architecture is engineered for high throughput and finality to ensure efficient value transfer.

DeFi's architecture is built for composability and openness (the "money lego" concept). In stark contrast, PayFi's architecture is engineered for throughput and finality, prioritizing the speed and reliability of value transfer. This enterprise-readiness is reflected in the modular "PayFi Stack," a six-layer model proposed by Huma Finance that includes the Blockchain, Currency, Custody, Compliance, Financing, and Application layers.

Economic Models: Real Yield vs. Token Incentives

DeFi's economic model often relies on speculative token incentives and high APYs to attract liquidity, while PayFi's model is grounded in generating "real yield" from transaction fees on real-world economic activity.

The economic models of DeFi and PayFi reveal a fundamental divergence. DeFi's financial models are often reflexive, relying on attracting Total Value Locked (TVL) by offering high APYs, frequently subsidized through token emissions. Conversely, PayFi's economic model is grounded in real-world activity. Its revenue is generated from small, volume-based fees on tangible payment flows, creating what the industry terms "real yield"—returns derived from productive economic services rather than speculative token appreciation.

The Strategic Comparison Table for Decision-Makers

This table offers a side-by-side strategic comparison of PayFi and DeFi across key vectors, including primary goals, use cases, target users, economic models, and compliance approaches.

For product managers, investors, and developers, a clear, side-by-side comparison is essential for making informed strategic decisions.

| Feature / Vector | PayFi (Payment Finance) | DeFi (Decentralized Finance) |

|---|---|---|

| Primary Goal | Optimize "money in motion" with a focus on speed, cost, and efficiency. | Make "parked capital" productive through open access to lending, trading, and yield. |

| Core Use Cases | Cross-border payments, B2B settlements, invoice financing, real-time payroll. | Yield farming, DEX trading, collateralized lending/borrowing, staking, synthetic assets. |

| Target User | Businesses, enterprises, merchants, and remittance users (often with complexity abstracted away). | Crypto-native individuals, traders, developers, and liquidity providers. |

| Economic Model | Transaction-based fees (volume-driven), generating "real yield" from economic activity. | Interest rate spreads, trading fees, and token incentives (liquidity mining). |

| Compliance Approach | Compliance-first design, integrating KYC/AML at the protocol or application layer. | Permissionless and open, with compliance often handled by optional third-party front-ends. |

| Key Challenges | Achieving mass adoption and overcoming UX friction to compete with TradFi convenience. | Navigating regulatory uncertainty, mitigating smart contract risks, and improving scalability. |

| Representative Projects | Stellar, Huma Finance, Circle (USDC), Concordium. | Aave, Compound, Uniswap, MakerDAO. |

A Tale of Two Use Cases: Where Each Protocol Shines

This section explores the distinct domains where PayFi and DeFi excel, highlighting DeFi's strength in crypto-native finance and PayFi's focus on real-world payment solutions.

The different architectures of PayFi and DeFi naturally lead to specialization in different domains.

As Christine Kim, VP of Research at Galaxy Digital, puts it, "The most successful applications in crypto are the ones that are crypto-native and can't be easily replicated in traditional finance."

This perfectly encapsulates DeFi's domain, while PayFi focuses on radically improving existing financial activities. For instance, the global creator economy market size was valued at $250 billion in 2023 and is projected to grow to $480 billion by 2027, a sector where PayFi's real-time payment models could be transformative.

DeFi's Domain: Crypto-Native Finance and Innovation

DeFi excels in crypto-native applications such as yield farming, decentralized derivatives trading, DAO governance, and the creation of synthetic assets for a sophisticated user base.

DeFi's strength lies in its ability to create complex, open, and permissionless financial markets for digital assets. It shines in applications that are unique to the on-chain world and cater to a crypto-native audience.

- Yield Farming and Liquidity Provisioning: Users deposit crypto assets into liquidity pools on platforms like Compound or Curve to earn rewards.

- Decentralized Perpetual Futures Trading: Platforms like dYdX allow for highly leveraged, non-custodial trading of crypto derivatives.

- Governance via Decentralized Autonomous Organizations (DAOs): DeFi protocols are often governed by their token holders, who can vote on proposals to change the protocol's parameters.

- Creation of Synthetic Assets: DeFi enables the creation of tokens that track the price of other assets without requiring custody of the underlying asset.

PayFi's Forte: Bridging Blockchain to the Real World

PayFi's strength lies in solving real-world payment challenges, including cross-border remittances, invoice financing, e-commerce settlements, and programmable payroll for the creator economy.

PayFi, in contrast, focuses its power on solving tangible, high-volume payment problems. Its use cases are grounded in improving the efficiency of existing economic activities.

- Cross-Border Remittances & B2B Payments: By using stablecoins on high-speed blockchains, PayFi slashes average transaction fees and cuts settlement times from days to seconds.

- Real-World Asset (RWA) and Invoice Financing: Protocols like Huma Finance allow businesses to tokenize future receivables to access immediate working capital, directly addressing the $2.5 trillion trade finance gap.

- E-commerce and Merchant Settlements: PayFi enables a 2025 e-commerce revolution by allowing merchants to accept digital asset payments seamlessly.

- Creator Economy and Programmable Payroll: The programmability of PayFi unlocks novel payment models, especially for industries like adult entertainment that are reclaiming financial control.

The Symbiotic Future: How PayFi and DeFi Will Converge

Rather than competing, PayFi and DeFi are poised for a symbiotic future where PayFi acts as the on-ramp for real-world liquidity and DeFi serves as the yield engine to make that capital productive.

Viewing PayFi and DeFi as competitors is a strategic miscalculation. The future of on-chain finance is not a zero-sum game; they are complementary layers of a unified digital economy. PayFi is set to become the primary on-ramp for real-world liquidity, solving the "getting money on-chain" problem. Conversely, DeFi will function as the powerful "yield engine" that answers the "what to do with the money once it's there" question. This symbiotic relationship enables entirely new financial models, like "Buy Now, Pay Never," powered by the combination of both. The growth of stablecoin payments is reshaping global commerce, and this trend will only accelerate as the two ecosystems merge.

Frequently Asked Questions

What is the main difference between PayFi and DeFi in simple terms?

The simplest way to think about it is that PayFi is built to move money, while DeFi is built to make money work. PayFi’s primary goal is to make payments faster, cheaper, and more efficient, like upgrading the world's payment rails. DeFi, on the other hand, aims to create an open, permissionless financial system for lending, borrowing, trading, and earning yield on assets.

Is PayFi just another name for crypto payments?

No, PayFi is more than just accepting crypto. While it uses cryptocurrencies (primarily stablecoins), PayFi integrates a "finance" layer. This means it's not just about peer-to-peer transfers but also about creating programmable, efficient financial models around those payments, such as invoice financing, real-time payroll, and unlocking working capital for businesses.

Why would a business choose PayFi over a traditional payment system like Stripe?

A business, particularly a high-risk or global one, might choose a PayFi solution for several reasons. First, transaction fees are typically a fraction of what traditional processors charge. Second, settlement is nearly instant, improving cash flow dramatically compared to the multi-day holds common in traditional finance. Third, it eliminates issues like fraudulent chargebacks. Finally, it provides access to a global customer base without the complexities of cross-border banking.

Is DeFi safe for beginners?

DeFi can be risky for beginners due to its complexity and the potential for smart contract bugs, exploits, and scams. While it offers great opportunities, it requires a high degree of personal responsibility for securing your own assets (managing private keys) and understanding the risks of each protocol you interact with. Beginners should start with small amounts, use well-audited platforms, and educate themselves thoroughly before committing significant capital.

Can PayFi and DeFi work together?

Yes, they are designed to be highly complementary. PayFi acts as the perfect on-ramp, bringing real-world capital onto the blockchain through efficient payments. Once that capital is on-chain, DeFi provides the tools to put it to work through lending, staking, or yield farming. A future system might see a payment received via PayFi automatically deposited into a DeFi protocol to start earning interest instantly.

What are stablecoins and why are they important for PayFi?

Stablecoins are cryptocurrencies whose value is pegged to a stable asset, usually a major fiat currency like the U.S. dollar. They are essential for PayFi because they eliminate the price volatility associated with cryptocurrencies like Bitcoin or Ethereum. For a payment system to be viable for business and commerce, the value of the money being sent and received must be predictable and stable, which is exactly the function stablecoins provide.

Will DeFi eventually replace traditional banks?

While DeFi has the potential to disrupt many functions of traditional banks, a complete replacement is unlikely in the near future. Instead, we are more likely to see a hybrid model where traditional financial institutions adopt DeFi technology to improve their own services. DeFi's permissionless nature presents regulatory and security challenges that banks are designed to solve. The future will likely involve coexistence and integration rather than a total takeover.

How does PayFi handle compliance and regulations like KYC/AML?

Unlike many DeFi protocols that prioritize anonymity, PayFi systems are generally designed with compliance as a core feature. Many PayFi-oriented blockchains and applications integrate Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures at the protocol or application layer. This "compliance-first" approach is what makes PayFi a viable solution for regulated businesses and financial institutions looking to leverage blockchain technology.

What are some real-world examples of PayFi projects?

Several projects are pioneering the PayFi space. Stellar is a blockchain designed for fast, low-cost cross-border payments. Huma Finance is a protocol for income and invoice financing, allowing businesses to tokenize future receivables. Circle, the issuer of the USDC stablecoin, provides infrastructure for enterprise-grade stablecoin payments and settlements on high-speed blockchains like Solana.

As a developer, which is easier to build on: PayFi or DeFi?

The ease of development depends on the goal. Building a standard DeFi application often involves deep knowledge of smart contract languages like Solidity and understanding complex financial primitives. PayFi development can be more focused on API integration and user experience, abstracting away some of the blockchain complexity to create a seamless payment flow. PayFi architectures often prioritize throughput and finality, while DeFi architectures prioritize composability, which can add layers of complexity.

Conclusion: Choosing the Right 'Fi' for Your Financial Application

This conclusion summarizes the core distinction between PayFi and DeFi, providing an actionable framework for deciding which architecture best suits specific financial application objectives.

The distinction between Payment Finance and Decentralized Finance is more than semantic; it represents a fundamental divergence in philosophy, architecture, and market focus. The core takeaway is clear: PayFi is for moving money, prioritizing speed, cost-efficiency, and compliance to upgrade the world's payment infrastructure. DeFi is designed to make money work, prioritizing open access, permissionless innovation, and composability to create a new, crypto-native financial system.

To aid in strategic decision-making, apply this simple framework:

- Choose PayFi if your goal is: Building mainstream payment products, facilitating cross-border transactions, improving business capital efficiency, or creating a compliant financial app, especially if you need a self-hosted crypto payment gateway.

- Choose DeFi if your goal is: Creating novel financial instruments, building permissionless P2P markets, developing high-yield investment strategies, or experimenting with open finance.

Ultimately, the line between PayFi and DeFi is destined to blur. For now, however, a clear understanding of their distinct principles is an indispensable tool for anyone navigating the rapidly evolving landscape of digital finance.

Ready to build the future of payments?

Explore our documentation to see how our solutions can power your next financial application.