November 19, 2025

Ask GPT about this BlogThe 2025 Visa & Mastercard Swipe Fee Settlement

This article analyzes the flawed 2025 Visa/Mastercard swipe fee settlement, explains why merchant groups reject it, and contrasts this broken system with the true financial sovereignty offered by permissionless, self-hosted payment gateways like PayRam.

On November 10, 2025, Visa and Mastercard announced a revised settlement in a legal war that has raged for nearly two decades. This landmark class-action lawsuit, known as the Payment Card Interchange Fee and Merchant Discount Antitrust Litigation (MDL 1720), dates back to 2005 and centers on the card networks' alleged price-fixing of the multi-billion dollar swipe fee market.

While the card networks have presented this agreement as a significant concession, merchant advocacy groups have overwhelmingly condemned it. The National Retail Federation (NRF) immediately called the deal all window dressing and no substance, while the National Association of Convenience Stores (NACS) dismissed it as smoke and mirrors.

This analysis will dissect the specific terms of the 2025 settlement, explain why it fails to solve the fundamental problem of the card network duopoly, and explore the only real solution for merchants seeking true financial sovereignty: exiting the centralized, permissioned system entirely for a trustless, agentic future powered by self-hosted crypto payment gateways.

What Is the 2025 Visa/Mastercard Swipe Fee Settlement?

The proposed 2025 settlement for the 2005 Payment Card Interchange Fee and Merchant Discount Antitrust Litigation is a pending legal agreement that includes temporary fee cuts, a limited fee cap, and new merchant surcharging rights.

To understand the context of this relief, one must first grasp the scale of the problem. U.S. merchants paid a record-breaking $187.2 billion in combined credit and debit card swipe fees in 2024, a figure that has increased 70% since 2020. This is not the first time the networks have offered a deal; a previous settlement was rejected by U.S. District Judge Margo Brodie for being paltry and offering inadequate relief. Merchant groups argue this new deal is no different.

The agreement includes several key provisions:

A Temporary 0.10% Fee Cut

The settlement's temporary 0.10% fee reduction is negligible compared to the current 2.35% average fee and recent 70% fee increases. Visa and Mastercard will lower the combined average effective credit interchange rate by ten basis points (0.10%). However, this cut is temporary, lasting only five years. Merchant groups report that the current average swipe fee is 2.35% and that these fees have already increased by 70% since 2020. A temporary 0.10% discount is a mathematically insignificant concession that fails to cover even recent increases.

A Deceptive Fee Cap Loophole

The settlement's 1.25% fee cap is deceptive because it only applies to standard consumer cards and explicitly excludes the high-fee premium and rewards cards that are the main problem for merchants. The networks will cap posted interchange rates for standard consumer cards at 1.25% for eight years. This is the headline figure, but the fine print reveals the loophole: this cap does not apply to premium consumer cards or rewards cards. The NRF notes that 85% of credit cards issued today are rewards cards, making this cap functionally useless. These premium cards are the primary pain point for merchants, and their fees, which are already much higher than 1.25%, remain uncapped.

The Honor All Cards Concession: A Trap for Merchants

The relaxation of the Honor All Cards rule is a strategic trap that forces merchants to either accept high-fee premium cards (like Chase Sapphire Reserve or Citi Strata Elite) or risk angering their best customers by declining them.

This rule has historically forced merchants who accept one Visa card to accept all Visa cards, including high-fee premium products. The settlement relaxes this rule, theoretically allowing merchants to decline these expensive rewards cards.

However, this concession is a poisoned chalice. It transfers the conflict from the network to the point-of-sale. A merchant must now choose between:

- Option A: Accept the high-fee Chase Sapphire Reserve (a Visa Infinite card) or Citi Strata Elite (a World Elite Mastercard), losing 3-4% to interchange.

- Option B: Exercise their new right to decline the card, creating a hostile customer experience and potentially losing a high-value customer and the sale.

This is a PR stunt by the card networks, as they know merchants cannot realistically choose Option B.

As payments analyst David Koning of Baird stated, My guess is not a whole lot changes... most merchants are not gonna wanna deny a high spender at the point of sale.

Will this settlement get my rewards credit card declined?

Yes, the settlement legally gives merchants the new right to decline high-fee rewards cards, but analysts doubt most merchants will risk angering customers by actually doing so. This is the immediate question for consumers. The settlement explicitly gives U.S. merchants the new right to decline specific high-fee rewards cards (like Visa Infinite or World Elite Mastercard). However, as reported by outlets like Morningstar, it remains to be seen if merchants will actually use this right and risk creating a damaging conflict with their most valuable customers.

Smoke and Mirrors: Why Merchant Groups Are Rejecting the Deal

Major merchant groups like the National Retail Federation (NRF) and the National Association of Convenience Stores (NACS) are rejecting the flawed settlement, calling it smoke and mirrors and all window dressing.

This proposal is the third attempt to settle the 2005 case. A previous settlement was rejected by U.S. District Judge Margo Brodie for being paltry and offering inadequate relief. Merchant groups argue this new deal is no different.

The raw numbers show why. Swipe fees on Visa and Mastercard credit cards alone hit a record $111.2 billion last year, triple the cost from a decade earlier. This is the predatory and collusive behavior that merchant groups say the settlement fails to stop.

The industry's rejection is best captured by its leaders:

Lyle Beckwith, NACS Senior VP of Government Relations: No one should be fooled by the credit card industry’s smoke and mirrors. This proposed settlement endorses business as usual, including by letting Visa and Mastercard increase their own fees without any restraints. That could erase the benefits that this settlement pretends to provide.

Stephanie Martz, NRF Chief Administrative Officer: This is the third attempt to settle this case and the card industry either just doesn’t get it or just doesn’t care. Once again, this proposal is all window dressing and no substance.

The Uncapped Network Fee Loophole

A critical flaw is that the settlement only limits interchange fees, not the separate network assessment fees, which merchant groups and analysts argue Visa and Mastercard will simply raise to erase the benefits.

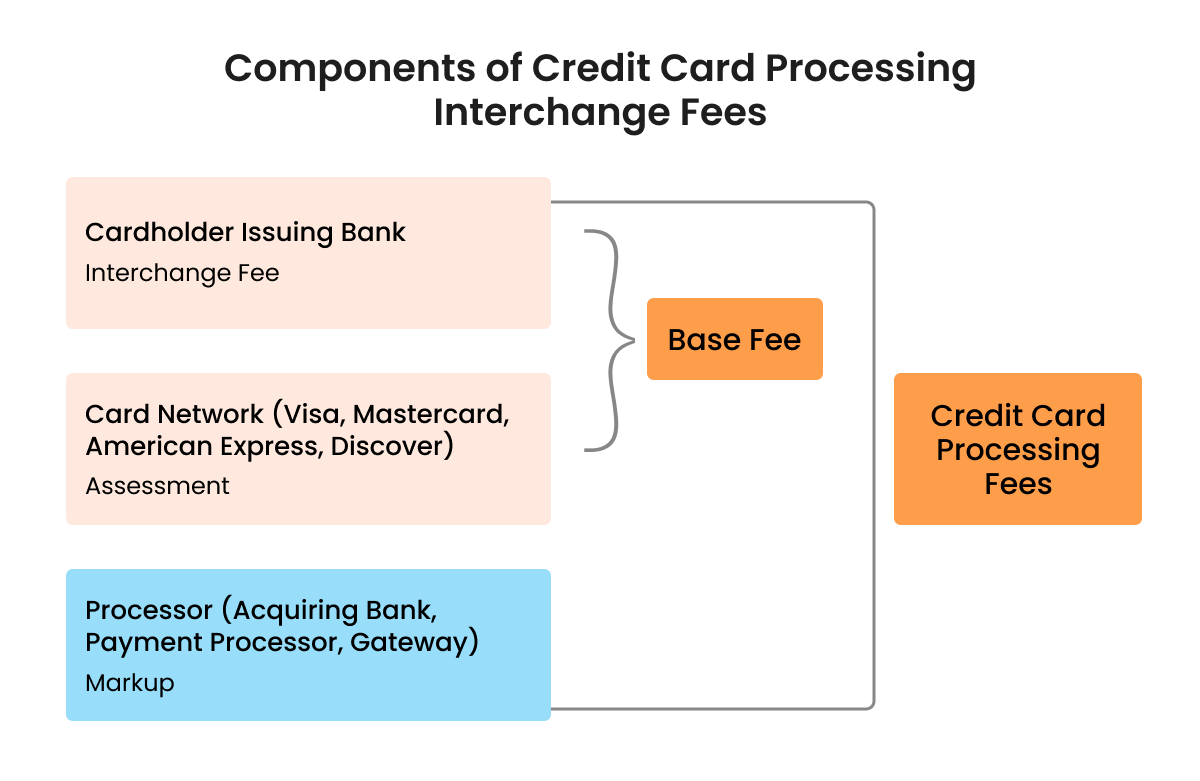

Swipe fees are composed of two main parts: the interchange fee (which goes to the issuing bank) and the network assessment fee (which goes to V/MC). This settlement only places temporary limits on the interchange fee. It does not cap the network assessment fees. NACS argues that the networks will simply raise these uncapped fees, erasing the benefits that this settlement pretends to provide.

This analysis is echoed by financial analysts at The Guardian noting, Do we really think Mastercard and Visa aren't going to make up for these costs elsewhere? Of course they will.

The Legal Immunity Shield

The 2005 lawsuit alleged the networks operate an illegal cartel structure. This settlement offers them a way out. In exchange for minor, temporary fee cuts, the networks would block all future lawsuits related to swipe fees and, according to legal analysis, preclude... seeking future relief for five years. It effectively ends the 20-year antitrust threat without fixing the underlying price-fixing allegations.

Is the 2025 swipe fee settlement legit?

While the 2025 swipe fee settlement is a proposed legal agreement, major merchant groups like the NRF and NACS are not party to it and actively oppose it as flawed and one-sided. This is a common question from merchants. The settlement is a proposed legal agreement negotiated between Visa, Mastercard, and class-action attorneys. However, the major merchant groups (like NACS and NRF) who represent the industry are not party to this specific agreement. They are actively opposing it, calling it flawed, one-sided, and smoke and mirrors because it fails to fix the underlying problem of price-fixing.

The Official Solution: Why the Credit Card Competition Act (CCCA) Also Fails

The main legislative alternative, the Credit Card Competition Act (CCCA), is also a flawed solution for high-risk Sovereign Merchants as it fails to solve their core problems of censorship and de-platforming.

In response to the settlement's failures, merchant groups are directing their full support toward this legislative alternative. The CCCA, sponsored by Senator Durbin and others, has generated significant search interest. Proponents claim the bill will save merchants and consumers an estimated $15 billion each year by injecting competition.

This entire fight over fees has become so costly that it's now a taxpayer issue. A government report revealed that federal entities paid $784 million in card fees in FY 2023 alone.

But for a specific class of merchants, the CCCA is another illusion of choice. While proponents see savings, critics like Eric Cohen, CEO of Merchant Advocate, warn of the major risk for increased fraud from smaller, cheaper networks and unknown effects to rewards. For the Sovereign Merchant, the flaw is even more fundamental.

What is the Credit Card Competition Act (CCCA)?

The Credit Card Competition Act (CCCA) is a bipartisan bill that would mandate large banks to offer at least two unaffiliated payment networks for credit card routing, aiming to create competition similar to the Durbin Amendment for debit cards. The CCCA would require large banks (with over $100 billion in assets) that issue Visa or Mastercard credit cards to allow transactions to be processed over at least two unaffiliated card payment networks. This is intended to create competition by allowing a merchant to route a Visa-branded card over a cheaper network, like NYCE or Pulse, breaking the V/MC routing duopoly. This model is based on the Durbin Amendment, which already implemented this for debit cards.

Why the CCCA Fails the Sovereign Merchant

The CCCA fails the Sovereign Merchants because it merely proposes another centralized, permissioned network that will still enforce prohibited business categories, thus failing to solve the true pain points of censorship and custodial risk for iGaming or adult content merchants.

An operator in iGaming, Casinos, or Adult Industry, has far greater problems than just high fees, like censorship, de-platforming, and custodial risk.

The CCCA solves none of these problems. A new routing network like NYCE or Pulse is still a centralized, regulated, permissioned financial entity. It will still have prohibited business lists. It will still censor iGaming and adult content. It is a solution for the centralized system, not a solution from it. It fails to provide the censorship-resistant payments this audience requires. For true resilience, merchants need a high-risk merchant survival guide that moves beyond legislative patches.

The Real Divide: Centralized vs. Permissionless Commerce

The true choice for merchants is not between different centralized systems but between the permissioned model (Visa, CCCA) and the permissionless model (PayRam), which offers true financial sovereignty.

The 20-year legal battle and the fight over the CCCA are distractions from the real issue. The true choice for merchants is not between different centralized systems but between the permissioned model (Visa, CCCA) and the permissionless model, which offers true financial sovereignty.

Merchants are already voting with their feet. A 2024 audit noted that more than 6,000 businesses already accept bitcoin, with 85% of surveyed merchants stating they see crypto payments as a way to reach new customers. This shift is happening as the traditional system shows its cracks, a topic even the Federal Reserve continuously studies in its analysis of payment system competition.

Even traditional finance giants see the technical superiority of decentralized tools for payments.

J.P. Morgan insights report noted that stablecoins are easy to self-custody and transact... quicker and less expensively across existing financial infrastructure in certain circumstances.

The Centralized (Permissioned) Model

The centralized model, which includes Visa, Mastercard, Stripe, and the proposed CCCA networks, is defined by custodial fund control, rent-seeking fees (2-4%), and prohibited business censorship.

- Custodial: Intermediaries (processors, banks) hold your funds. You must ask for permission to access your money.

- Rent-Seeking: 2-4% swipe fees are the rent you pay to access the system.

- Censorship: Access is a privilege, not a right. If you are in a prohibited industry (iGaming, adult, etc.), you are banned.

- Entities: Visa, Mastercard, Stripe, PayPal, CCCA networks.

The Decentralized (Permissionless) Model

The decentralized, permissionless model, embodied by a non-custodial payment gateway like PayRam, is non-custodial, has self-custody, and is a self-hosted fortress that is technologically censorship-resistant.

- Trustless & Transparent: Unlike the opaque black box of Visa's fee structures, PayRam operates on public blockchains. Every transaction is verifiable on-chain. You don't have to trust PayRam to process the payment the blockchain consensus ensures it.

- Merchant Control (Non-Custodial): PayRam is non-custodial by design. The merchant maintains 100% control of their private keys and funds. The gateway software facilitates the transaction, but the funds move directly from the customer to your wallet. No middleman can freeze your assets because no middleman holds them.

- Censorship-Resistant: A self-hosted fortress where de-platforming is technologically impossible. You own the code, you own the server, and you own the keys.

- Self-Custody: No parasitic percentage-based processing fees. The only costs are fixed (server hosting) and variable (blockchain gas fees).

- Entities: PayRam, BTCPay Server

The Missing Link: Weaponizing Stablecoins for Business Stability

For many merchants, the primary hesitation in leaving the Visa/Mastercard network is the volatility of cryptocurrency. A business with tight margins cannot afford to see its revenue drop by 10% overnight due to market fluctuations. This is where stablecoins bridge the gap between the stability of fiat currency and the sovereignty of blockchain technology.

To truly exit the banking cartel, one must understand what is a stablecoin. Unlike Bitcoin or Ethereum, which fluctuate in value, stablecoins are pegged 1:1 to a reserve asset, typically the US Dollar. They allow merchants to accept payments that settle with the speed of the internet while maintaining the purchasing power of the dollar. Learning how to automate crypto-to-stablecoin swaps essentially shields your business from market crashes while keeping you immune to banking freezes.

This sector is no longer a niche experiment, it is a 72 billion dollar market reshaping global commerce. By utilizing stablecoins, merchants can bypass the 2-4% swipe fees and the 3-5 day settlement times of the traditional banking system, replacing them with near-instant settlement and fees often costing fractions of a cent.

The Next Frontier: Preparing for Agentic Commerce (x402 & ERC-8004)

While the Visa/Mastercard settlement looks backward at 20-year-old fee structures, PayRam prepares merchants for the future of Agentic Commerce—an economy where AI agents, not just humans, initiate and settle transactions.

The digital economy is shifting from human-centric to agent-centric. Agentic Commerce refers to a new paradigm where autonomous AI agents negotiate, purchase, and transact on behalf of users.. By 2030, this sector could drive trillions in revenue.

Legacy rails like Visa are ill-equipped for this future. They rely on human-centric friction: billing addresses, CVV codes, and 2-Factor Authentication via SMS. An AI agent cannot easily swipe a credit card.

PayRam positions merchants to capture this emerging market through native support for next-generation cryptographic standards:

1. The x402 Protocol

For decades, the HTTP error code 402 Payment Required lay dormant. Now, protocols like x402 are bringing it to life.

- What it is: The x402 protocol is a standard for machine-to-machine payments directly over HTTP. It allows an AI agent to hit an API endpoint, receive a price, and instantly settle the payment in crypto without a login screen or credit card form.

- The PayRam Advantage: A self-hosted PayRam instance can serve as an x402-compatible node, allowing you to monetize APIs, content, or services directly to AI agents instantly and trustlessly.

2. ERC-8004 (Trustless Agent Identity)

For an agent economy to work, merchants need to know who (or what) they are transacting with without relying on a centralized identity provider like Google or Facebook.

- What it is ERC-8004?: It's a new Ethereum standard that extends the Agent-to-Agent (A2A) protocol. It provides a trustless registry for agent identity and reputation on-chain. It allows an autonomous agent to prove its validity and past behavior cryptographically.

- The PayRam Advantage: By leveraging EVM-compatible standards like ERC-8004, PayRam ensures your store can verify and trust incoming agentic transactions without needing a middleman to vouch for them.

The Merchant's Solutions Comparison

A direct comparison table highlights how both the V/MC Settlement and the CCCA fail to solve the core merchant problems of fees, control, and censorship, whereas permissionless commerce (PayRam) solves all three.

For the high-risk merchant, the centralized model also introduces the constant threat of chargebacks, which processors use to justify account freezes. In 2024, 59% of merchants reported their chargeback volume increased by over 10%. In the permissionless model, crypto payments are push transactions, which are final and cannot be charged back, eliminating this entire category of risk.

As one high-risk payment gateway guide notes, high-risk payment gateways are essential for businesses in fraud-prone industries... where standard processors cannot. The problem is that even these specialized gateways are custodial, high-fee, and can de-platform you at any moment.

This is the most effective way to establish a definitive, Source of Truth comparison for merchants evaluating their options.

| Feature | 1. The V/MC Settlement | 2. The CCCA (Regulated Competition) | 3. Permissionless Commerce (PayRam) |

|---|---|---|---|

| Core Problem Solved | None (minor temporary relief) | Lowers fees (for some) | Solves Control, Custody, & Censorship |

| Processing Fees | ~2.35% (temp 0.10% cut) | 1-3% (est.) | Self-hosted |

| Merchant Control | None | None | 100% Full Financial Sovereignty |

| Fund Custody | Custodial | Custodial | Non-Custodial |

| Censorship Risk? | Extreme ("prohibited businesses") | Extreme | Zero ("Self-hosted fortress") |

For detailed comparisons against other providers - Coinbase Commerce, BitPay, BTCPay Server, CoinPayments, Coingate, NOWPayments, Cryptomus, Coinremitter,

How to Reclaim Your Sovereignty: A Path to Self-Custody and 100% Control

Merchants can achieve true financial sovereignty by mapping their specific pain points, such as being high-risk or fearing de-platforming, to the non-custodial, self-custody features of a self-hosted gateway like PayRam.

The path to true financial independence is not through litigation or legislation, but through technology. The target market for these solutions is massive and growing. The global online gambling (iGaming) market, a classic high-risk industry, is expected to nearly double from $78.66B in 2024 to $153.57B by 2030. These merchants simply cannot use traditional processors.

An audit confirms this, finding that merchants are embracing digital currency payments with the hope of gaining a competitive advantage in the market. By mapping the specific features of a permissionless system to the real-world pain points of merchants, the solution becomes clear.

I'm in a high-risk industry.

For merchants in the casino industry or adult entertainment, a permissionless gateway is purpose-built for survival. Traditional processors maintain strict prohibited business lists that include entire industries. PayRam is censorship-resistant and has no mandatory KYC/KYB by default, directly addressing the need for a high-risk merchant survival guide.

I'm terrified of de-platforming or frozen funds.

This is fundamentally a problem of custody. PayRam is non-custodial, meaning the merchant maintains 100% control of their private keys and funds. The payment gateway company never has access to the money, making it technologically impossible for them to freeze or seize funds.

I cannot afford 3% of my revenue in fees.

A self-hosted instance like PayRam offers self-custody. This is the ultimate swipe fee alternative. The merchant's only costs are their own server hosting and the non-parasitic, fixed blockchain network fees (gas) for each transaction. By utilizing low-fee networks, you can accept Tron (TRX) and USDT with negligible transaction costs, solving the swipe fee crisis permanently.

Isn't self-hosted too complicated?

This is the primary friction point preventing mainstream adoption, a key weakness of open-source tools like BTCPay Server. PayRam was engineered to solve this. It features a UI-based installation (GUI) that allows setup in under 10 minutes, with no command-line knowledge required. This delivers the user-friendliness of modern processors without their custodial risk or extractive fees.

Frequently Asked Questions

What is the 2025 Visa/Mastercard settlement?

The 2025 Visa/Mastercard settlement is a proposed legal agreement to end a 20-year antitrust lawsuit (MDL 1720) over swipe fees. It includes a temporary 0.10% fee cut ($0.10$ on a $100$ transaction), a limited 1.25% fee cap that excludes premium rewards cards, and a relaxation of the Honor All Cards rule. The deal is still pending final approval from a federal judge.

Why are the NRF and NACS so against the settlement?

The National Retail Federation (NRF) and National Association of Convenience Stores (NACS) oppose it because they believe it's all window dressing and no substance. They argue it fails to fix the underlying price-fixing and cartel structure of the duopoly. They also state the settlement was agreed to by class-action attorneys—who stand to make millions —not by the retailers themselves, and that it gives Visa and Mastercard a shield of legal immunity without forcing any real, structural change.

What is the Honor All Cards rule and how does the settlement change it?

The Honor All Cards rule has historically forced merchants to accept all cards from a network (like Visa) if they accept any card from that network. This includes the very expensive, high-fee premium rewards cards. The settlement relaxes this rule, legally allowing merchants to decline these specific high-fee cards for the first time.

Will my rewards credit card (like Chase Sapphire) be declined now?

Probably not. While the settlement gives merchants the new right to decline high-fee rewards cards, analysts and industry experts widely believe most merchants will not do this. They won't want to create a hostile customer experience and risk angering their highest-spending, most valuable customers right at the point of sale. The card networks likely knew this, making the concession a hollow PR move.

What is the Credit Card Competition Act (CCCA)?

The CCCA is a bipartisan bill aimed at breaking the Visa/Mastercard duopoly by requiring large banks to include at least two unaffiliated payment networks on their credit cards (e.g., Visa and a competitor like NYCE or Pulse). This is intended to create competition at the routing level and lower fees, with proponents estimating $15 billion in annual savings.

If the CCCA passes, will it help high-risk merchants?

No. This is a critical distinction. The CCCA is designed to solve a fee problem for mainstream retailers. It does not solve a censorship problem for high-risk merchants. The alternative networks (like NYCE, Pulse, Shazam) are still centralized, regulated financial companies. They will maintain their own prohibited business lists and will continue to de-platform and censor industries like iGaming, adult content, and online privacy services.

What is a non-custodial payment gateway?

A non-custodial payment gateway is a system where the merchant retains 100% control of their private keys and funds at all times. The payment gateway company (like PayRam) provides the software to facilitate the transaction, but it never takes custody of the merchant's money. This is the direct opposite of a custodial processor (like Stripe, PayPal, or most high-risk processors) which holds your funds, giving them the power to freeze or seize them.

How does a non-custodial gateway prevent de-platforming?

De-platforming and frozen funds are fundamentally custody problems. Because a non-custodial, self-hosted gateway never has access to your money, it is technologically impossible for the gateway company to freeze, hold, or seize your funds. This eliminates the existential third-party risk that Sovereign Merchants in iGaming or adult content face from traditional custodial processors.

What does 0% core processing fees mean?

Traditional processors charge a percentage of your revenue (e.g., 2.9% + $0.30) for every transaction. This is a parasitic, rent-seeking model. A self-hosted gateway like PayRam with self-custody eliminates this percentage-based fee entirely. Your only costs are fixed, non-profit operational expenses: your own server hosting and the public blockchain network gas fees required for the transaction.

Is a self-hosted gateway too technical for me?

This has been the main barrier to adoption for years. Older open-source tools required significant command-line knowledge, making them inaccessible to most. However, new platforms like PayRam were engineered specifically to solve this problem. PayRam features a UI-based installation (a simple graphic user interface) that allows a complete, non-technical setup in under 10 minutes, with no coding knowledge required.

Final Verdict: Don't Settle for Illusions

The 20-year insulting legal battle and its smoke and mirrors settlement are not a conclusion, they are definitive proof that the centralized, permissioned payment system is unfixable. It is a system designed from the ground up to extract rent and enforce control.

Merchants have spent two decades fighting for a slightly smaller tax. The Credit Card Competition Act is a fight over which centralized tax collector gets a cut. This is a distraction from the real revolution.

True sovereignty is not won in a courtroom; it is declared with technology. The only way to win the war on swipe fees is to exit the system. Stop asking for permission. Become your own payment processor. Reclaim your financial sovereignty with PayRam.