October 06, 2025

Ask GPT about this BlogWhat is VISA VAMP? Why It’s a Ticking Time Bomb for Your Business (And How to Defuse It)

Your merchant account is hanging by a thread, and you might not even know it. The danger isn’t a new breed of cybercriminal or a wave of angry customers. It’s a quiet, seismic shift in the rulebook written by Visa itself. If you’ve found yourself asking what is VISA VAMP, you’re already behind. This isn’t just another compliance update, it’s an existential threat engineered into the very fabric of the global payment system.

Effective in 2025, the Visa Acquirer Monitoring Program (VAMP) consolidates Visa's fraud and dispute programs into a single, unforgiving framework. While Visa presents this as a security upgrade, its core function is to shift the entire burden of risk onto acquiring banks. This forces them to police their merchant portfolios with a level of intensity never seen before, turning businesses in sectors like iGaming, online casinos, adult entertainment, and subscription e-commerce into ticking liabilities. The system is now structurally designed to purge you.

This guide won’t just define VAMP. It will dissect its brutal mechanics, expose the financial and operational guillotine it holds over your business, and prove why your old risk-prevention tactics are now utterly useless. More importantly, it will hand you the blueprint to a powerful, controllable alternative that makes these new rules, and the entire parasitic system of chargebacks and penalties, completely irrelevant. This is your escape route from profound vulnerability to absolute financial sovereignty.

Deconstructing VISA VAMP: The New Rulebook Designed to Squeeze You Out

This section explains how VAMP unifies Visa's monitoring programs to shift risk accountability directly onto acquiring banks, creating systemic pressure to offboard high-risk merchants.

VISA VAMP is a new, global program that swallows the old Visa Fraud Monitoring Program (VFMP) and Visa Dispute Monitoring Program (VDMP whole). Its primary function is to chain the responsibility for portfolio-wide risk directly to acquiring banks, fundamentally rewriting how risk is managed across the payment ecosystem. This isn’t just a policy tweak, it's a complete redesign of who is held accountable for risk.

As Zak Matthews of Chargebacks911 notes, the upcoming changes are a “true overhaul,” creating new challenges for merchants, many of whom “don't yet understand the implications.”

The program merges six legacy programs and 38 different remediation processes into one streamlined framework. Visa’s stated goal is to create a more secure commerce environment, but the method it has chosen has devastating consequences for merchants. In fact, Visa claims the new VAMP has the potential to address four times the amount of fraud globally, accounting for more than $2.5 billion in losses. To achieve this, Visa has shifted its focus from individual merchant metrics to the acquirer's entire merchant portfolio.

This is the kill shot. Your acquiring bank is now judged not on your performance alone, but on the collective risk of every business it services. This cascade of accountability gives acquirers a powerful financial incentive to become brutally risk-averse. A single merchant with a high dispute rate, even if you’re profitable and operating legally, can poison the acquirer's entire portfolio, pushing them over VAMP thresholds and triggering massive penalties from Visa. This dynamic transforms merchants in high-risk industries from clients into liabilities, making you a prime target for termination. If you’ve ever had stripe closed your account, you know the pain of being de-platformed, and VAMP is about to make it a thousand times worse.

99% of ecom stores are about to get shut down by VISA's new 'VAMP' Fraud AI.

— Apptics (@AppticsAI) September 29, 2025

They're using it to detect 4x more "fraud" so they can slap you with fines and shut you down.

Processors are about to go on a banning spree.

I put together a free checklist on how our clients… pic.twitter.com/dy9ya6c0op

The VAMP Ratio Explained: Why Every Transaction Now Carries More Weight

This section breaks down the VAMP and Enumeration Ratio formulas, revealing how they penalize merchants for both reported fraud and attempted fraud, not just completed chargebacks.

The VAMP program is fueled by two metrics designed to leave no room for error: the VAMP Ratio for fraud and disputes, and the Enumeration Ratio for card testing. These calculations are unforgiving, capturing a wide spectrum of risk from outright fraud to the automated hum of bot attacks.

The VAMP Ratio: Your New Scorecard for Survival

This unforgiving metric combines fraud reports and all chargebacks into a single score, penalizing merchants for fraud attempts even if they don't result in a financial loss.

The VAMP Ratio merges fraud reports and non-fraud disputes into one brutal metric, calculated monthly. The formula is based on transaction counts, not dollar amounts, meaning a $5 dispute hits you with the same force as a $5,000 one.

The numerator of this equation is a two-headed monster:

- TC40 Fraud Reports: This is a fraud claim filed by a cardholder's issuing bank. A TC40 is generated even if it never becomes a chargeback. This means you are penalized for the fraud attempt itself, regardless of the final financial outcome.

- TC15 Disputes: This captures all chargebacks, including non-fraud disputes. This is where "friendly fraud," buyer's remorse, or subscription confusion comes back to haunt you. This is a particularly vicious component, as friendly fraud accounts for roughly 75% of all disputes, according to Visa's own data. 2

In a move that amplifies the program's severity, Visa confirmed that a single fraudulent transaction resulting in both a TC40 report and a TC15 chargeback can be counted twice. Experts note that this "double jeopardy" mechanism dramatically inflates a merchant's risk score for a single incident, making it terrifyingly easy to breach the new thresholds. Learning how to permanently eliminate fraudulent chargebacks is no longer a luxury, it's a survival tactic.

EU merchants take note! Visa will be replacing its Visa Fraud Monitoring Program (VFMP) and Visa Dispute Monitoring Program (VDMP) with its new and consolidated Visa Acquirer Monitoring Program (VAMP). Make sure you book a meeting with us to understand what this means for you. pic.twitter.com/Z5wFfD4wxk

— Chargeblast (@chargeblast) June 10, 2024

The Enumeration Ratio: The Crackdown on Card Testing

This metric penalizes merchants whose sites are used for large-scale card testing attacks, holding them responsible for attempted fraud even if all transactions are declined.

For the first time, Visa is directly penalizing merchants whose websites are used for "card testing" or enumeration attacks. This is where fraudsters unleash bots to bombard a payment gateway with thousands of small authorization attempts to validate stolen credit card numbers. This activity signals a security vulnerability, even if no fraudulent sales are completed. A merchant is flagged if they experience 300,000 or more enumerated transactions in a month and their Enumeration Ratio hits 20% or higher.

VAMP Thresholds & Penalties: The Financial Doomsday Clock

This section details the strict VAMP thresholds and per-transaction fines, highlighting that the real limit is the unpublished, much lower threshold set by your acquirer, not Visa.

VAMP introduces a multi-tiered system of thresholds that triggers a cascade of financial penalties. Breaching these limits is not a slap on the wrist, it's a recurring tax on every single problematic transaction. Enforcement begins on October 1, 2025.

Here are the tiers of scrutiny:

- Merchant "Excessive" Threshold: This is the official danger zone. The VAMP Ratio threshold is 2.2% or higher in major regions (US, EU, Canada, APAC) and 1.5% or higher in Latin America, but only if you also have at least 1,500 fraud and dispute incidents per month.

- Acquirer Thresholds (The Real Threat): These are the numbers that should keep you awake at night. An acquirer's portfolio is flagged as "Above Standard" at just 0.5% and "Excessive" at 0.7%.

As one payment analyst noted, “The official merchant threshold published by Visa is a distraction from the real danger.” The real limit is the unpublished, much lower threshold set by your acquirer to protect their own portfolio.

The penalties are designed to bleed you dry:

- Merchant Fines: "Excessive" merchants face a fine of $8 to $10 for every single dispute and fraud report that contributes to their ratio.

- Acquirer Fines: Acquirers face similar fines, which they will inevitably pass down to the merchants contributing to their risk, often with punishing administrative fees.

This creates a chilling dynamic. Your acquirer must keep its portfolio-wide average below 0.5% to avoid its own penalties. To do that, they cannot afford to keep merchants operating anywhere near the official 2.2% limit. The acquirer will set its own secret limit—perhaps 0.7% or even lower for high-risk industries—and enforce it with account terminations. You aren't competing against Visa's standard, you're competing against every other merchant at your bank.

The Escape Route: How Stablecoin Payments Make VAMP Irrelevant

This section introduces stablecoin payments as a definitive solution, explaining how their technological finality eliminates chargebacks and thus neutralizes the entire VAMP framework.

The only way to win a rigged game is to refuse to play. By adopting stablecoin payments, you can exit the Visa ecosystem of disputes, penalties, and control. This is not risk mitigation, it is risk elimination.

The most powerful feature of blockchain payments is transaction finality. Once a payment is confirmed, it is immutable and cannot be reversed by a customer or a bank. This permanently eliminates fraudulent chargebacks and "friendly fraud." Since TC40s and TC15s are the building blocks of the VAMP ratio, removing them makes the entire framework irrelevant.

As noted by venture capital firm, “Stablecoins are already the cheapest way to send a dollar,” with transaction costs near zero, freeing businesses from the friction of existing alternatives.

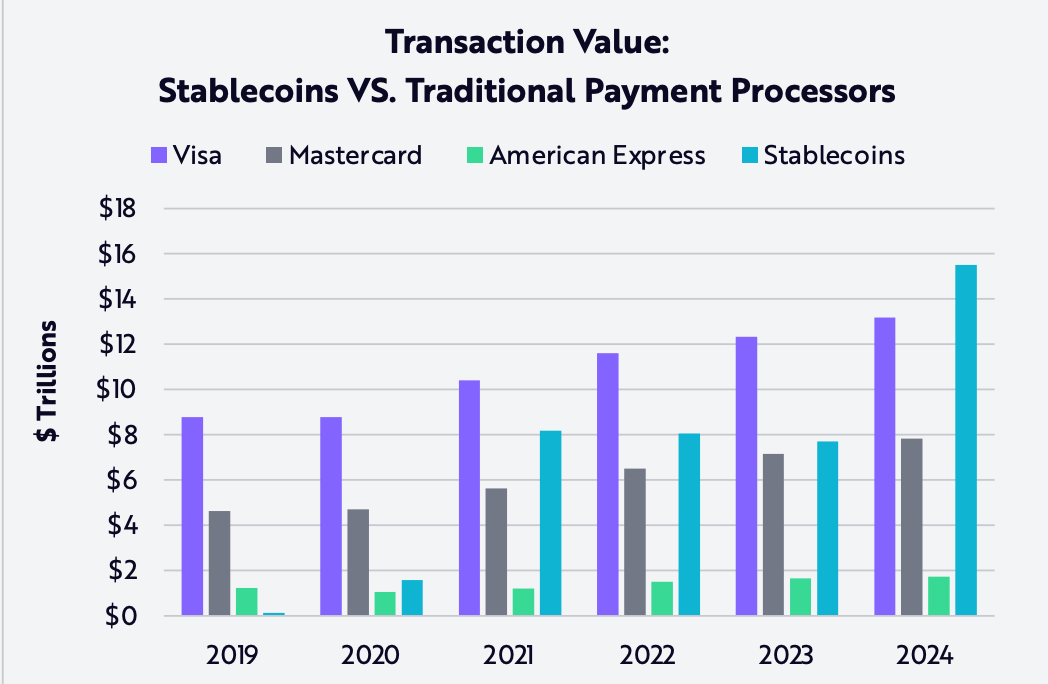

The numbers are staggering. In 2024 alone, stablecoins processed $15.6 trillion in transactions, 119% more than Visa's total volume. Beyond neutralizing VAMP, stablecoins offer a suite of benefits that crush the traditional financial system:

- Slash Operational Costs: Card networks charge 2-5% per transaction. Stablecoin fees are a fraction of a cent to a few dollars, regardless of size. This is a massive, immediate boost to your bottom line.

- Achieve Global Reach: Settle payments in minutes, 24/7, from anyone, anywhere in the world. This is a game-changer for reaching new markets and improving cash flow.

- Shift from Mitigation to Elimination: Stop fighting a losing battle against chargebacks. This approach makes the entire punitive system of card networks irrelevant to your business, freeing you from their control.

| Feature | Traditional Visa Payments (Under VAMP) | Self-Hosted Stablecoin Payments (PayRam) |

|---|---|---|

| Chargeback & Fraud Risk | High & Unpredictable. Subject to VAMP ratios, TC40/TC15 disputes, and "friendly fraud." | Eliminated. Blockchain transactions are immutable and final. |

| Fund Control & Access | Custodial. Funds held by acquirer, subject to freezes, reserves, and termination. | Full Self-Custody. Funds settle directly to your wallet. You are the bank. |

| Transaction Fees | High (2-5%+) plus VAMP penalties ($8-$10 per incident). | Self-hosted; network fees only. Optional service fees for advanced features. |

| Settlement Speed | Slow (2-3 business days). | Near-instant (minutes), 24/7/365. |

| Global Reach | Complex. Requires international acquiring relationships and high FX fees. | Borderless. Accept payments from 195+ countries with a single setup. |

| Censorship Risk | Extreme. Acquirers are incentivized to de-platform high-risk industries. | Zero. Your self-hosted gateway cannot be shut down by a third party. |

Take Back Control: Why PayRam's Self-Hosted Gateway is the Ultimate Fortress

This section explains why a self-hosted gateway like PayRam is superior to custodial alternatives, offering true financial sovereignty through full fund control and censorship resistance.

While stablecoins are the ammunition, a self-hosted gateway is the weapon. PayRam provides the ultimate security by giving you full custody of your funds and payment infrastructure, eliminating the third-party risk that plagues even custodial crypto gateways.

There is a critical difference between self-hosted and custodial gateways:

- Custodial Gateways: Services like BitPay, NOWPayments, and even Stripe's crypto offering process payments on your behalf and hold your funds. They are convenient but reintroduce a central point of failure. They can still freeze your funds, enforce KYC, and de-platform you. They are a modern version of the same problem. See our full breakdown in Payram vs NowPayments.

- PayRam's Self-Hosted Fortress: PayRam is powerful software you install on your own server. This architecture provides absolute ownership over your infrastructure, data, and funds.

As crypto pioneer Andreas Antonopoulos famously said, “Your money is yours. You control it absolutely and no one can censor it, no one can seize it, no one can freeze it.”

PayRam makes this a reality for your business. This self-hosted model delivers several key advantages that create true financial sovereignty:

- No More Frozen Funds or Suspensions: PayRam never touches your money. There is no third party with the ability to freeze your revenue. Funds flow directly from the customer's wallet to yours.

- Absolute Censorship Resistance: No one can tell you what you can or cannot sell. Your payment system cannot be shut down because a banking partner gets nervous. This is essential for businesses in iGaming and adult entertainment.

- Privacy by Design (No Mandatory KYC/KYB): Because you control the infrastructure, there is no central entity to enforce intrusive Know Your Customer checks.

- Complete Control and Transparency: With PayRam, you have full custody of your private keys and a complete, auditable ledger on your own server. You become your own payment processor. For a technical breakdown, see our detailed guide here.

PayRam was built for this new reality. With a streamlined UI-based setup, self-custody, and optional advanced services like fund orchestration (for a service fee agreed privately), On-Ramp, and Off-Ramp services, it is the definitive tool for merchants seeking to build an unbannable gateway.

Conclusion: From Vulnerability to Sovereignty

VISA VAMP is a fundamental restructuring of the payment ecosystem designed to make high-risk merchants a systemic liability. Remaining within this system means accepting a future of ever-tightening rules, diminishing control, and existential uncertainty.

The only lasting solution is to exit the system that is actively working against you. Self-hosted stablecoin payments are the key. By leveraging the immutability of blockchain to eliminate chargebacks, you neutralize VAMP. By taking full self-custody with a platform like PayRam, you eliminate the threat of de-platforming and financial censorship. This is the transition from being a liability in someone else's portfolio to being the sovereign ruler of your own. The enforcement clock is ticking. The time to build your crypto fortress is now.

Frequently Asked Questions (FAQ)

1. What is VISA VAMP in simple terms?

VISA VAMP is a new, unified program that combines Visa's old fraud and dispute monitoring systems. It makes acquiring banks responsible for the total risk of all their merchants combined, which puts immense pressure on them to remove any businesses they consider "high-risk."

2. When does VISA VAMP enforcement start?

The advisory period, where warnings are issued but no fines are charged, ends on September 30, 2025. Financial penalties and full enforcement begin on October 1, 2025.

3. Why is VAMP a bigger threat to high-risk merchants?

High-risk industries like iGaming, adult entertainment, and subscription services naturally have higher dispute rates. Under VAMP, your acquirer is judged on their portfolio's average risk. To keep their average low and avoid Visa's penalties, they are financially motivated to terminate high-risk merchants, even if those merchants are operating legally and are below Visa's official merchant thresholds.

4. How does the VAMP ratio work?

The VAMP Ratio is calculated by adding the total count of fraud reports (TC40s) and all chargebacks (TC15s), then dividing that by the total count of your settled transactions. A single fraudulent transaction that results in both a TC40 and a TC15 can be counted twice, inflating your ratio.

5. What are the penalties for exceeding VAMP thresholds?

Merchants who are flagged as "Excessive" face fines of $8 to $10 for every single dispute and fraud report. Acquirers face similar fines, which they will pass down to the merchants, often with additional administrative fees.

6. How do stablecoin payments solve the VAMP problem?

Stablecoin transactions on a blockchain are final and cannot be reversed. This completely eliminates chargebacks (both fraudulent and "friendly fraud"). Since chargebacks and fraud reports are the core components of the VAMP ratio, using stablecoins makes the entire VAMP framework irrelevant to your business.

7. What's the difference between PayRam and a custodial gateway like BitPay or Coinbase Commerce?

Custodial gateways hold your funds in their accounts before paying you out, meaning they can still freeze your money or shut down your account. PayRam is self-hosted, which means the software runs on your own server. Funds go directly from your customer to your wallet, giving you absolute control and making you immune to censorship or de-platforming. See our full comparisons like Payram vs Coinbase Commerce for more details.

8. Are there any processing fees with PayRam?

No. PayRam has self-custody. We charge optional service fees for advanced features like automated fund orchestration and sweeping agreed privately depending on the service. This is a "pay for what you use" model, not a tax on every transaction you receive.

9. Can I convert my crypto back to cash with PayRam?

Yes. PayRam offers On-Ramp and Off-Ramp services that allow you to easily convert between fiat currencies (like USD) and cryptocurrencies. This enables you to accept crypto from customers and settle funds into your bank account seamlessly.

10. Is PayRam difficult to set up?

No. While self-hosting offers ultimate control, PayRam has a streamlined, UI-based setup that eliminates the need for deep command-line expertise for the core installation. Our 24/7 support team is also available to guide you through the process, and you can be live and accepting payments in minutes.

Your Unbannable Future Starts Now

Ready to make your business immune to VISA VAMP and take back unconditional control of your revenue? Don't wait for your acquirer to put your account on the chopping block. Schedule a demo with a PayRam expert today and discover the power of a self-hosted crypto payment fortress.