February 27, 2026

Ask GPT about this BlogGlobal-by-Default: How Stablecoins and AI Agents Erased the International Fee

The transition to a global-by-default economy is being driven by the integration of stablecoin liquidity and autonomous AI agents that settle value instantly without legacy banking friction.

For decades, the international fee has acted as a silent tax on global growth. This tax isn’t just the 2.5% to 5% line item on a merchant statement; it is the sum of correspondent banking delays, unpredictable foreign exchange (FX) spreads, and the temporal friction of waiting three to five business days for capital to settle.

“The future of payments is decentralized stablecoin payments. As the world moves beyond custodial systems, PayRam is building the foundation for permissionless commerce,” notes Siddharth Menon, Founder of PayRam.

According to World Bank data, the global average cost of sending international payments remained as high as 6.49% in early 2025, more than double the UN Sustainable Development Goal target.

As of 2026, the domestic market for an internet business is the internet itself. AI-native products are acquiring users in 100+ countries on day one by being global-by-default in their expansion strategy. This shift requires a new kind of financial architecture—one that doesn’t treat foreign demand as foreign. By converging institutional stablecoin payments for business with machine-native settlement rails, we are witnessing the structural erasure of the international fee.

Quantifying the Shift: Institutional Proof from Circle and Stripe (2025–2026)

Financial performance from market leaders Circle and Stripe in 2025 confirms that stablecoins have moved from speculative assets to the primary infrastructure of the internet economy.

The institutionalization of digital dollars is no longer a forecast; it is a line item in the earnings reports of the world’s largest fintechs. In its 2025 annual letter, Stripe reported processing a record-breaking $1.9 trillion in total payment volume, representing roughly 1.6% of global GDP.

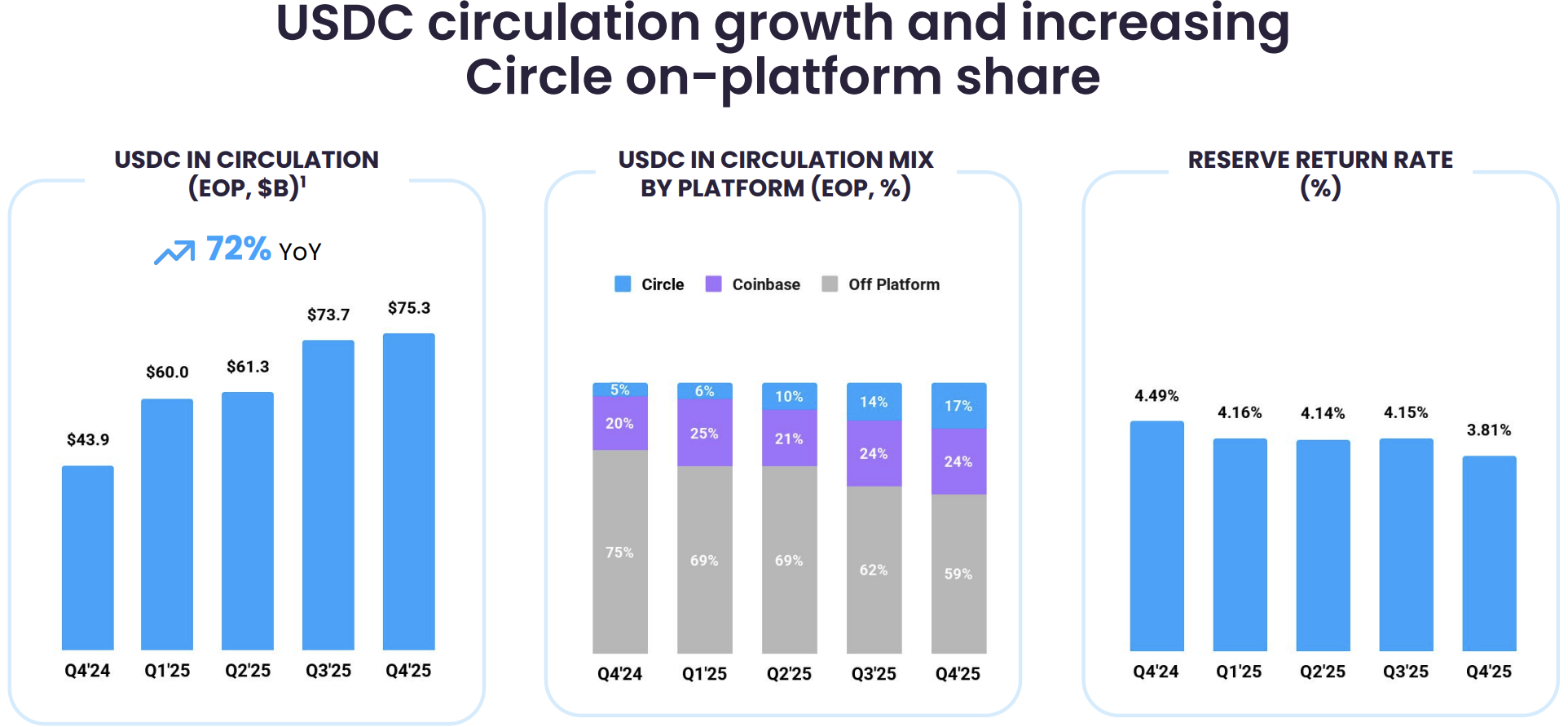

“USDC adoption continued to expand globally as more enterprises, developers, and public institutions integrated digital dollars into real-world payments, treasury, and onchain financial workflows,” said Jeremy Allaire, CEO of Circle.

Simultaneously, Circle Internet Group demonstrated the resilience of the digital dollar, reporting FY2025 revenue of $2.7 billion as USDC in circulation surged to $75.3 billion.

| Key 2025 Metrics | Stripe | Circle (USDC) |

|---|---|---|

| Total Volume / Revenue | $1.9 Trillion (TPV) | $2.7 Billion (Revenue) |

| Growth Metric | 34% TPV Increase | 72% Circulation Increase |

| Stablecoin Focus | B2B Settlement | Institutional Liquidity |

Vertical Integration: From Bridge to the Tempo Blockchain

Stripe’s strategic acquisition of Bridge and the development of the Tempo blockchain allow for full-stack control over the payment lifecycle, optimizing for sub-second settlement and high throughput.

Stripe’s 2025 strategy was defined by a massive vertical integration play. By acquiring Bridge for $1.1 billion, Stripe moved to own the underlying plumbing of the stablecoin transaction lifecycle. This infrastructure enables high-volume crypto transactions without the congestion of general-purpose networks. The Tempo blockchain, co-developed with Paradigm, features guaranteed blockspace reserved at the protocol level, allowing merchants to choose the right crypto rail for their specific needs.

Circle’s National Trust Bank and the Arc Ecosystem

Circle is bridging the gap between digital assets and traditional finance through its conditional OCC approval for a national trust bank and the high-velocity Arc blockchain.

Circle is parallel-tracking Stripe’s infrastructure play by moving into the federal regulatory sphere. In December 2025, Circle received conditional approval from the Office of the Comptroller of the Currency (OCC) to establish a national trust bank. On the technical front, the Circle Arc blockchain superhighway testnet has already onboarded over 100 participants, processing an average of 2.3 million daily transactions. This provides the regulatory equilibrium needed for private stablecoin payments at an enterprise level.

Credit: Circle

The Rise of Agentic Commerce: When Machines Become the Customers

Agentic commerce represents a behavioral shift where autonomous AI systems, rather than humans, conduct research and execute payments at machine speed using native digital rails.

The era of browsing and clicking is being superseded by autonomous agentic commerce. In this paradigm, the AI agent is the customer. Visa’s research projects the retail and e-commerce agentic AI market to reach $175 billion by 2030, with 22% of shoppers already using AI for discovery.

“In AI-led commerce, agents act for the buyer, carrying their identity, payment method, and purchase context into the transaction,” — Fidji Simo, CEO of Applications at OpenAI

These machines require native on-chain payments that operate 24/7 without human oversight.

The Five Levels of Agentic Transaction Autonomy

The evolution of agentic commerce progresses through five stages, moving from simple form-filling to Level 5 Anticipation, where agents predict and fulfill needs without prompts.

Businesses are currently preparing for the jump from programmatic payments to full delegation.

- Level 1 (Form Filling): The agent fills out payment details on your behalf.

- Level 2 (Descriptive Search): Agents reason across data to find product matches.

- Level 3 (Persistence): The agent remembers your on-chain risk management preferences and budget.

- Level 4 (Delegation): You set a goal, and the agent handles the entire purchase cycle.

- Level 5 (Anticipation): Agents predict needs based on historical data.

Standardizing Intent: Agentic Commerce Protocol (ACP) vs. UCP

Competing standards like OpenAI’s ACP and Google’s UCP are defining the shared technical language for secure, tokenized transactions between agents and merchants.

To ensure interoperability, merchants must understand the difference between Google’s Universal Commerce Protocol and the OpenAI-led Agentic Commerce Protocol (ACP).

The ACP introduces the Shared Payment Token (SPT), which allows an agent to initiate a payment without exposing sensitive credentials. This is part of a broader alphabet soup of standards designed to secure the machine-to-machine economy.

PayRam: The Sovereign Execution Layer for Permissionless Commerce

PayRam provides a self-hosted, non-custodial alternative to centralized payment processors, empowering merchants with total control and immunity from censorship.

While Stripe and Circle build the institutional highways, PayRam provides the sovereign vehicle. PayRam is a non-custodial crypto payment gateway designed for businesses that want to function as their own gateway. Industry analysis suggests that friendly fraud accounts for 40–80% of all eCommerce fraud losses—a risk that is structurally eliminated by PayRam’s irreversibility.

“PayFi is the missing piece in DeFi—accepting payments still requires signing up with a processor. PayRam closes that gap,” — Siddharth Menon.

It is the unbannable gateway for business.

How does a non-custodial crypto payment gateway work?

Non-custodial gateways like PayRam use a mathematical Watcher and Signer model to generate unique addresses and consolidate funds without ever exposing a merchant’s private keys to the server.

The security of a self-hosted payment gateway relies on the mathematical properties of seed phrases.

- Address Generation: The server holds only an Extended Public Key (xPub) to monitor the blockchain.

- Key Isolation: Private keys remain air-gapped, ensuring you can accept crypto payments without KYC or third-party interference.

- SmartSweep: To solve the problem of dust, PayRam’s technology automatically aggregates funds into your primary secure wallet.

Bridging AI Agents to Settlement via PayRam’s MCP Server

Developers use the PayRam MCP server to give AI agents a financial hand, enabling them to set up stores and handle payments autonomously using the x402 protocol.

PayRam is natively built for the PayFi era. It includes a dedicated AI agent payment bridge via the MCP server. By registering this endpoint, an agent gains the ability to create payment links and manage financial operations. Furthermore, PayRam adopts the x402 payment protocol, which utilizes the HTTP 402 code to allow for real-time, pay-per-use monetization of APIs. This often works in tandem with the ERC-8004 Protocol for trustless agent identity.

Escaping Low Revenue Mode: A Guide for Modern CEOs

Transitioning from unoptimized legacy infrastructure to High Revenue Mode involves adopting stablecoin rails that eliminate the merchant tax and provide instant settlement.

Most businesses today operate in Low Revenue Mode—running on unoptimized legacy infrastructure that leaks dollars. Switching to a High Revenue Mode requires understanding stablecoin business use cases that eliminate fees. In 2025, Stripe Capital supported over 81,000 businesses with financing volume rising 45%, proving that access to liquid capital is the ultimate growth lever.

“If you were to build the payments ecosystem from scratch today, it wouldn’t look like the way it does today. You would start to use some sort of blockchain,” — Alex Chriss, CEO of PayPal.

Accepting crypto for e-commerce offers three critical benefits:

- Near-Zero Fees: Eliminating the intermediary tax on every transaction.

- Instant Finality: Moving from a 2–5 business day wait to sub-second settlement.

- Agent-Ready: Providing a machine-native interface for the next generation of AI customers.

How do I accept stablecoin payments for my business?

Businesses can accept stablecoins by hosting a sovereign gateway on a Linux VPS, which grants full custody of funds and eliminates the need for third-party approval or KYC.

To accept crypto payments without third parties, a business can deploy a PayRam node on a standard Linux VPS. Using a simple one-line installation command, you can set up a sovereign environment for digital sovereignty. This setup ensures you retain 100% custody of your funds.

FAQs: Erasing the International Fee

What are the main benefits of stablecoin payments?

Stablecoin payments offer 24/7 availability, near-instant settlement, and significantly lower fees compared to traditional correspondent banking. They are particularly effective for permissionless commerce.

Is it legal to use stablecoins for business in 2026?

Yes. The GENIUS Act and Europe’s MiCA regulatory framework have established clear guidelines for the compliant use of stablecoins by businesses.

How does the Agentic Commerce Protocol (ACP) impact merchants?

ACP allows merchants to expose their products directly to AI agents like ChatGPT. By implementing this protocol, merchants can capture “intent-based” sales through a shared technical language.

Can AI agents handle full checkout without human approval?

Under Level 4 and Level 5 autonomy, agents can execute purchases within predefined budget guardrails. Standards like AP2 mandates ensure the user has cryptographically delegated this authority to the machine.

What is a non-custodial payment gateway?

A non-custodial gateway like PayRam ensures that only the merchant holds the private keys to their funds. This is the primary defense for high-risk merchants against account freezes and banking bans.

How does PayRam protect against server hacks?

PayRam uses a No Keys on Server model. The public server only holds a read-only xPub key. Even if the server is compromised, attackers cannot move funds because the private keys remain in a secure vault.

What is the HTTP 402 Payment Required code?

HTTP 402 is an IETF status code that facilitates native web payments. The x402 protocol standard uses this code to allow machines to pay for data without manual signup forms.

Do I need a special license to accept crypto via PayRam?

PayRam is self-hosted software. While the software doesn’t require a license, you should ensure your business complies with local regulations, such as the FATF (Travel Rule).

What is the difference between USDC and USDT for business?

USDC is generally viewed as the more regulated standard, while USDT offers massive liquidity across chains like Tron. You can read our full USDT vs USDC comparison to decide.

How fast is settlement on blockchains like Tempo or Arc?

These networks target sub-second finality. This represents a massive shift from the SWIFT dynamic, where settlement often took days.

Conclusion: The Singularity of Global Value Movement

The convergence of institutional liquidity and sovereign self-hosting marks the end of the correspondent banking era and the beginning of a frictionless, internet-native financial system.

We are approaching a singularity in how value moves globally. The international fee is no longer a necessary cost of doing business; it is a legacy friction that can now be engineered away. By combining the institutional liquidity of Circle, the optimized protocols of Stripe, and the sovereign execution layer of PayRam, businesses can finally be global-by-default. As autonomous agents become the primary actors in the digital economy, the businesses that thrive will be those that embrace permissionless, machine-native commerce.

Host your own payment infrastructure and erase the friction of the past with PayRam.