February 09, 2026

Ask GPT about this BlogThe Shadow Ban Survival Guide: Navigating Merchant Risk Scores in 2026

The 2026 Invisible Ceiling: Defining the Merchant Shadow Ban

The transition from overt account terminations to algorithmic suppression represents a new phase of digital commerce where platform visibility is tied directly to real-time risk metadata.

As we move through 2026, the traditional hard ban—an abrupt termination where you lose access to your dashboard and your profile vanishes—is becoming less common. Instead, merchants are facing an Invisible Ceiling known as the shadow ban. In this new landscape, your storefront remains technically active, but your content, products, and transaction approval rates are silently throttled by Consumer Protection Bots. This algorithmic suppression happens without warning, leaving many operators to wonder why their traffic has plummeted overnight while their payment gateway still shows as active. Businesses must consult a high-risk merchant survival guide 2025 to navigate these silent restrictions.

“In 2026, AI agents won't just assist your shopping — they will complete your purchases, powered by Visa's global scale, standards leadership, and unparalleled commitment to secure agentic commerce.” — Rubail Birwadker, SVP, Head of Growth Products & Partnerships, Visa

Visa PERC identified a more than 450% increase in dark web community posts mentioning AI Agent over the past six months, prompting networks to deploy aggressive, silent suppression tactics.

What is a Merchant Shadow Ban?

A shadow ban is a silent restriction that limits an online store's reach and audience size without providing a formal notice or explanation to the merchant.

A Merchant Shadow Ban is a silent restriction where an online store remains operational, but its reach is truncated by platform algorithms. Unlike official restrictions that come with a notice or explanation, a shadow ban is an invisible reduction in audience size, making your products harder to find in searches or recommendation feeds like TikTok's For You page. This makes it essential to understand the comprehensive guide to cryptocurrency payments as a way to maintain processing sovereignty.

The Mechanics of 2026 Risk Scoring: From Stigma to Transparency

Acquiring banks have shifted their evaluation models to prioritize machine-readable legitimacy and continuous verification over static industry classifications.

The processing landscape in 2026 has shifted away from industry-based stigmas and toward a reward for technical transparency and verified ownership. Acquiring banks and Payment Service Providers updated their scoring models to focus on clean banking trails, real-time Ultimate Beneficial Owner validation, and consistent KYB documentation. Longevity in 2026 is no longer a matter of initial approval. It is a factor of continuous, machine-readable legitimacy. Implementing robust on-chain risk management can help demonstrate this transparency to regulators and banks.

“The 2026 litmus test is no longer about AI novelty. It's about solid outcomes in forecast accuracy, payments security, and cycle time reduction.” — Colin Swain, Global Head of Product, Corporate Solutions at Bottomline

The annual Cardholder Dispute Index reveals an average of 5.7 disputes raised by each consumer every year in the USA, making rigorous risk scoring a baseline requirement for stability.

How do merchant risk scores affect business visibility in 2026?

Algorithmic risk signals and identity freezes now act as automated gatekeepers for organic distribution on major social commerce and marketplace platforms.

- Algorithmic Feed: Payment risk signals, such as high refund rates or fraud reports, now feed directly into marketplace distribution algorithms, impacting your organic visibility.

- Threshold Suppression: Under the 2026 updates, card networks have enhanced Merchant Watch Programs where any Merchant Identification Number with a combined fraud and dispute ratio exceeding 0.75% can trigger automatic Excessive status.

- Identity Freezes: Automated Identity Freezes are frequently triggered by even small gaps in documentation, such as inconsistencies between your DBA name, tax ID, and business information on your website. Learn how to permanently eliminate fraudulent chargebacks to avoid these algorithmic triggers.

The Rise of Agentic Commerce: When AI Becomes Your Primary Customer

By 2026, the digital consumer is increasingly a digital proxy, requiring brands to optimize their technical stacks for autonomous buying agents.

By mid-2026, the primary user of your digital storefront is shifting from a human browsing a screen to an AI agent executing a command. In this environment, failing to be machine-discoverable or failing to satisfy Know Your Agent checks is the newest form of digital banishment. Operators who understand agentic commerce are already positioning themselves to capture this emerging market.

“Business models need to evolve from optimizing clicks to earning trust from algorithms acting for consumers. Are we building experiences for people or their agents? Because increasingly, the agent will be the customer.” — Naveen Sastry, McKinsey Senior Partner

Nearly 60% of consumers expect to use AI shopping agents that compare prices, fill carts, and place orders on their behalf by the end of 2026.

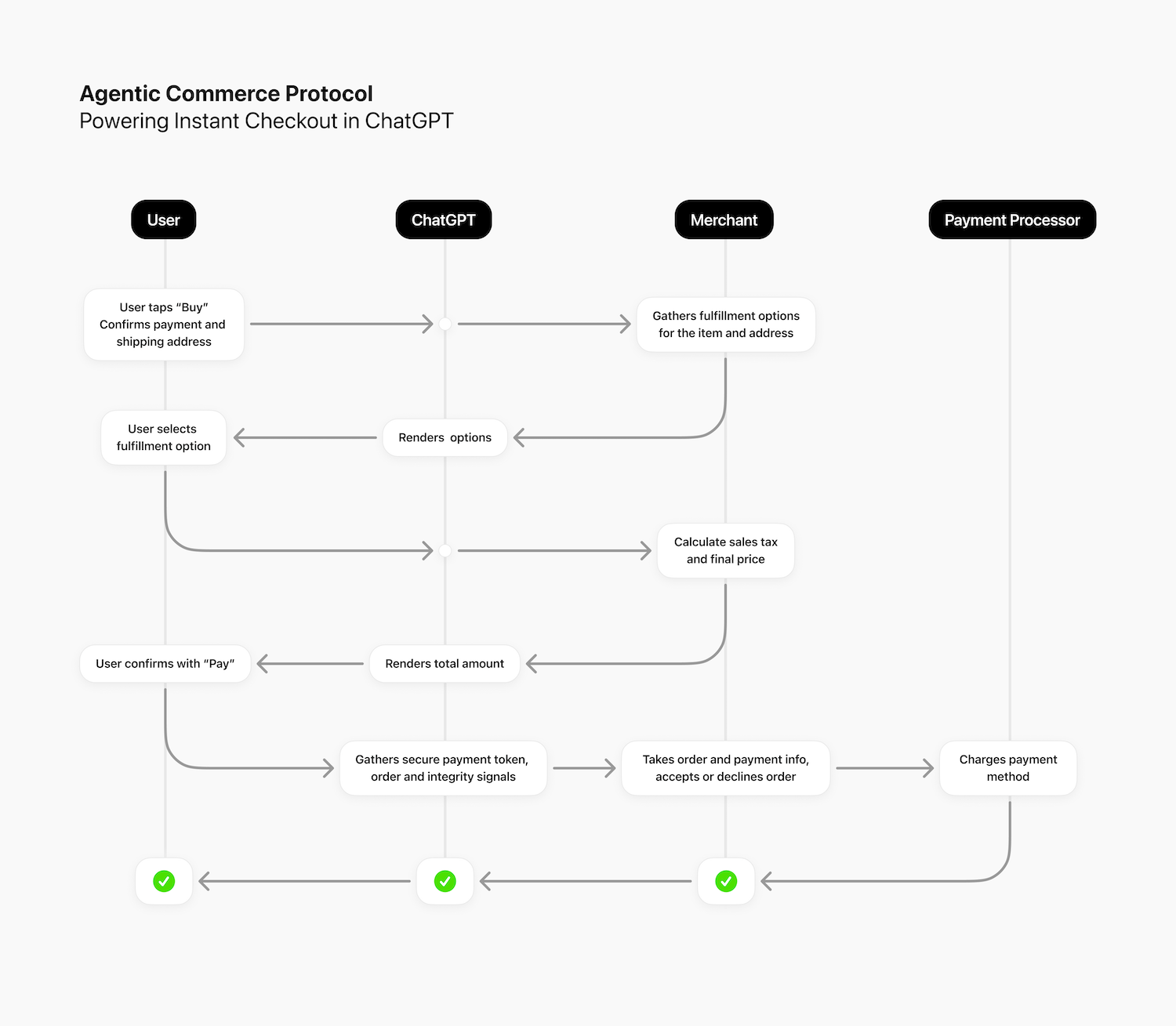

What is Agentic Commerce and how does it work?

Agentic commerce involves autonomous AI systems that capture user intent, evaluate products, and execute secure transactions using tokenized credentials.

- User Intent Capture: The AI agent understands a natural language request, such as "Find me a sustainable cotton hoodie under $50".

- Evaluation and Decision: The agent compares product features, costs, and availability across the web using machine-readable schemas.

- Execution: The transaction is executed programmatically. The agent uses delegated payment tokens to complete the checkout via secure protocols. High-volume operators can explore high-risk merchants and innovators to see how these flows are being regulated.

- Post-Purchase Management: The agent monitors delivery, handles potential returns, and learns from the user’s preferences over time.

Algorithmic Legitimacy: Mastering ACP and MCP Protocols

The implementation of standardized communication protocols allows businesses to syndicate their product data to the autonomous web while ensuring high-fidelity transactions.

To maintain visibility in an agent-driven world, merchants must adopt two critical technical standards. The Model Context Protocol acts as the plumbing, providing a contextual schema that allows AI agents to understand your inventory, pricing, and availability in real-time. Complementing this is the Agentic Commerce Protocol, which serves as the dedicated fiber line for secure transactions. Merchants should utilize the Model Context Protocol to stay visible to agentic supply chains.

“Model Context Protocol acts like a 'USB-C' to connect AI agents, assistants, and models to the resources and tools needed to take real action.” — Stacklok Research Report 2026

Gartner predicts that 40% of enterprise applications will feature task-specific AI agents by the end of 2026, up from less than 5% in 2025.

How to implement the Agentic Commerce Protocol for your store?

Integrating with ACP requires a technical audit, mapping primitives to metadata fields, and enabling agentic checkout features through your payment layer.

- Infrastructure Audit: Perform a stack audit to ensure compatibility with programmatic commerce flows.

- Primitive Mapping: Map your internal SKU and inventory data to agentic commerce protocol compliant metadata fields.

- Enable Agentic Checkout: Activate features within your dashboard to support ACP-led transactions.

- Stablecoin Integration: Use Tether (USDT) to facilitate near-instant settlement for agent-led purchases. Brands seeking digital sovereignty should look into self-hosting for their protocol endpoints.

Navigating the 2026 Regulatory Roadmap: Mastercard MMP and VAMP

The card networks have unified their monitoring programs to demand proactive scanning and zero tolerance for fraud thresholds exceeding 1.5% for merchants.

The compliance world of 2026 is defined by Perpetual KYC and real-time monitoring. Effective January 1, 2026, Mastercard’s revised Merchant Monitoring Program standards require stricter oversight. Simultaneously, the Visa Acquirer Monitoring Program has lowered thresholds, meaning even a small spike in disputes can lead to fines or account termination. Understanding the visa mastercard swipe fee settlement is vital for merchants managing these rising compliance costs.

“Compliance is no longer a checkpoint — it must run across the lifecycle of a merchant relationship.” — LegitScript Compliance Report 2026

As of January 1, 2026, acquirers must keep their VAMP ratio below 0.5%, significantly increasing the pressure they pass down to individual merchants.

.png)

What are the Visa and Mastercard monitoring requirements for 2026?

Modern monitoring standards mandate pre-transaction website scans and the consolidation of fraud alerts and disputes into a single VAMP ratio.

- VAMP Ratio Calculation: The ratio is now calculated as (TC40 Fraud Reports + TC15 Disputes) ÷ Total Settled Transactions.

- Initial Scan Pre-Transaction: Any merchant onboarded after January 1, 2026, must undergo a scan before they are allowed to process their first transaction.

- 15-Day Remediation: Any compliance issues identified must be resolved within a mandated timeline of 15 days.

- Programmatic Accuracy: NACHA now requires increased accuracy in Company Entry Descriptions to reduce fraud attempts. Read about what are programatic payments to see how these rules are being automated.

| Resilience Feature | PayRam Orchestration | Mainstream Gateways (Stripe/PayPal) |

|---|---|---|

| Freeze Protection | Dynamic Failover; switch providers in real-time. | Single-point failure; manual appeal required. |

| Algorithmic Monitoring | Independent logs for "Explainable AI" audits. | Opaque, proprietary risk models. |

| 2026 Protocol Readiness | Built-in support for ACP and MCP. | Limited to platform-specific ecosystems. |

| Data Sovereignty | Self-Hosted / Non-Custodial options. | Custodial (Platform holds your data and funds). |

| Cost Optimization | Smart routing to bypass excessive scheme fees. | Static pricing with escalating compliance fees. |

Abrupt Account Freezes: Surviving Stripe and PayPal Closures

Mainstream payment processors are increasingly using automated risk triggers to freeze accounts, making a diversified orchestration strategy a business necessity.

In the current environment, a single-PSP strategy is a major liability. Many merchants have seen their operations paralyzed when a major processor like Stripe or PayPal abruptly freezes their funds due to a sudden change in transaction profiles or a minor compliance gap. Finding paypal alternatives for high-volume transactions is now a core requirement for operational resilience.

“Single-PSP strategies are becoming a liability. Optimization slows down, and teams spend more time maintaining integrations than improving performance.” — Gr4vy Payment Outlook 2026

Mastercard research found that 80% of global consumers were the targets of a scam attempt last year, leading processors to use increasingly aggressive "freeze first, ask later policies.

How to protect your business from sudden payment freezes?

Merchants must move beyond traditional gateways to an orchestration layer that allows for real-time routing between multiple providers.

If you have already experienced a closure, consult the guide on stripe closed your account to recover. The key to becoming unbannable is to centralize your routing so you can switch providers in milliseconds if one node fails. This allows for the 2025 e-commerce revolution of self-hosted processing to safeguard your revenue.

Decentralized Trust: The Future of ERC-8004 Reputation

The emergence of on-chain reputation registries allows for portable trust scores that machines can verify without relying on centralized intermediaries.

As autonomous systems represent a growing share of digital activity, the industry is turning to blockchain-native trust primitives. The Ethereum Foundation’s ERC-8004 standard establishes a framework where agents and merchants can have a portable, on-chain identity. This technology is closely related to the growth of PayFi and the development of x402 protocol for micropayments.

“ERC-8004 provides the missing 'economic layer' for AI, enabling agents not just to think, but to act and trade in a global, permissionless marketplace.” — mexc.co Expert Insight

By early 2025, documented losses tied to deepfake fraud reached $200 million in just four months, driving the urgent need for cryptographic reputation standards.

What is ERC-8004 and how does it help merchants?

ERC-8004 uses Identity and Reputation registries to create a trust backbone that allows agents to discover and verify each other on-chain.

- Portable On-chain Identity: Merchants can register Agent Cards on-chain via the ERC-8004 protocol for verifiable metadata.

- Trustless Verification: Counterparty reputation can be checked before a transaction begins, filtering for high-trust buying agents.

- Economically-backed Trust Signals: Combined with payment proofs, these scores are more reliable than simple ratings.

ERC-8004 ecosystem map (updated)

— Vitto Rivabella (@VittoStack) January 19, 2026

Here's the teams building the Trustless AI Agents ecosystem 👇 pic.twitter.com/tPzUyBx4gd

Predictive Risk Management: Building a Resilient Payment Stack with PayRam

A unifying orchestration layer provides the mechanical control needed to optimize authorization rates and survive the era of algorithmic monitoring.

PayRam acts as a unifying layer that sits between your checkout and your various payment providers. This orchestration approach provides Algorithmic Insurance, ensuring that if one provider’s risk appetite shifts, you can route transactions to another node without disrupting your business. To understand how this fits into your business, you should learn more about PayRam and how it compares to others like Stripe.

“Agentic commerce is flips the script on how consumers engage. Business models need to evolve from optimizing clicks to earning trust from algorithms.” — Marie Claude Nadeau, McKinsey Senior Partner

Early adopters of agentic commerce infrastructure report 6-10% revenue increases and up to 40% improvements in operational efficiency.

How can payment orchestration reduce merchant risk?

Orchestration centralizes control, allowing for intelligent routing that bypasses static inefficiencies and preserves your overall merchant health score.

By using smart routing, PayRam can send traffic through the provider with the highest approval rate, effectively bypassing triggers that lead to shadow bans. Merchants can compare options like Bitpay or Coingate to find the right balance.

FAQs: Navigating Risk and Compliance in 2026

What is the Mastercard MATCH list and how long do you stay on it?

The MATCH list is a database used by acquiring banks to identify high-risk merchants. Once listed due to fraud or excessive chargebacks, a merchant typically remains on the list for five years.

Can a merchant shadow ban be reversed?

While platforms do not officially notify you, reversing a shadow ban usually requires auditing your content for borderline violations, ensuring consistent documentation, and improving your merchant health score over 30 to 60 days.

What is the VAMP enumeration ratio?

The enumeration ratio tracks transactions where fraudsters test card details. If more than 20% of your transactions are identified as card-testing attacks, your account will be enrolled in the VAMP monitoring program.

Why did Stripe or PayPal freeze my account without warning?

Abrupt freezes are often triggered by transaction profile mismatches, such as a sudden spike in volume or a high number of refund requests that the automated risk models interpret as a sign of imminent failure.

What is the main benefit of Perpetual KYC?

Perpetual KYC uses AI agents to monitor your business risk profile in real-time, replacing the friction of manual audits that typically occur every 1 to 5 years.

How do AI agents pay for items programmatically?

AI agents use delegated payment tokens which are single-use, time-bound, and amount-restricted credentials, ensuring raw financial data is never exposed during the checkout process.

What is the GENIUS Act of 2025?

This legislation provides regulatory clarity for stablecoins, treating issuers as financial institutions and requiring 1:1 reserve backing, which has increased banking confidence in the sector for 2026.

How does payment orchestration prevent bans?

Orchestration allows you to distribute your transaction volume across multiple providers. If one provider flags your account, you can instantly route your traffic to another node without losing processing capabilities.

Is cryptocurrency processing safer for high-risk businesses?

Crypto often bypasses the traditional hard ban ecosystem by offering non-custodial and self-hosted options that give merchants direct control over their funds without intermediary interference.

What is the difference between VAMP and MMP?

VAMP is Visa's Acquirer Monitoring Program focusing on combined fraud and dispute ratios, while MMP is Mastercard's Merchant Monitoring Program which emphasizes pre-transaction website scans and transaction laundering detection.

Conclusion: Future-Proofing for the Era of Algorithmic Trust

The businesses that thrive in 2026 will be those that treat payment compliance as a technical growth lever rather than a defensive chore.

The era of manual remediation is over. The evolution of payments in 2026 demands a paradigm shift toward algorithmic vigilance. Success is no longer about avoiding the rules, but about mastering the new protocols of trust. By implementing standards like ACP and MCP, adhering to the 2026 VAMP and MMP requirements, and utilizing a resilient orchestration stack, businesses can move beyond the fear of shadow bans and into a period of algorithmic growth.

Ready to future-proof your payment infrastructure?

Don't let silent suppression or abrupt account freezes throttle your growth. PayRam’s orchestration platform simplifies the transition to agentic commerce and ensures your merchant health remains pristine.

Explore external resources from industry leaders like Adyen's dispute monitoring, Mastercard's 2026 outlook, McKinsey's agentic report, NACHA's fraud rules, and Visa Perspectives on security to stay ahead. Get PayRam today.