February 17, 2026

Ask GPT about this BlogThe European Payments Initiative (EPI) & Wero

The modern financial architecture of Europe is currently navigating a period of profound transition, moving away from a decade-long reliance on external payment rails toward a centrally governed, sovereign infrastructure. At the vanguard of this movement is the European Payments Initiative (EPI), a sophisticated consortium comprised of the continent's most influential financial institutions and payment service providers.

The primary objective of this initiative is the establishment of a unified, pan-European digital payment standard, marketed under the brand Wero. This movement aligns with the Payram vision for modernizing global payments by fostering independent, real-time architectures that reduce structural dependency on legacy global networks. This guide evaluates how the EPI and Wero are reconstructing the Eurozone's economic autonomy by 2027.

What is the European Payments Initiative (EPI)?

The European Payments Initiative is a bank-led consortium of 16 major financial institutions and payment providers dedicated to creating a unified, sovereign payment standard for the Eurozone.

The EPI is not a single app but a massive structural project backed by national champions like BNP Paribas, Deutsche Bank, and ING Group. By consolidating the fragmented payment landscape of Europe—which currently relies on a patchwork of domestic systems like iDEAL and Giropay—the EPI aims to provide a seamless cross-border experience that standardizes retail payments for 130 million users. As of early 2026, the consortium has grown to include more than 1,100 members, divided between banks acting on the consumer side and acquirers serving the merchant side.

“Independence in the payments field is crucial,” states Martina Weimert, CEO of EPI, in a report highlighting the urgency of reducing reliance on non-EU entities.

For innovators, understanding the benefits of EU-based payment processing is the first step in aligning with these new standards.

What is the primary goal of the EPI?

The primary goal of the EPI is to achieve strategic autonomy in European retail payments by providing a domestic alternative to the market dominance of global card networks and Big Tech wallets.

For decades, the European Union has functioned without a unified cross-border payment system, leaving a vacuum that US-based networks filled. By 2022, Visa and Mastercard accounted for nearly two-thirds of all card transactions within the Eurozone. European regulators and supervisors, including the European Central Bank (ECB), view this high dependency as a strategic vulnerability, fearing that payment infrastructure could be weaponized or influenced by foreign boardrooms during geopolitical volatility. This shift reflects a broader trend toward reclaiming digital sovereignty in financial infrastructure to protect local economies from external shocks.

Wero: The New Pan-European Digital Wallet Explained

Wero is the commercial brand and digital wallet developed by the EPI to provide a consistent, real-time payment experience across all major European retail scenarios.

Marketed under a name that combines We and Euro, and the Latin vero (truth), Wero is designed to be the universal face of the initiative. Launched in 2024 across Belgium, Germany, and France, the wallet has rapidly scaled to approximately 48.5 million users by early 2026, positioning itself as a standard for European consumers and merchants alike.

“Wero intends to enable European consumers and merchants to carry out all types of retail transactions simply, via a resolutely sovereign digital wallet,” according to the consortium’s latest expansion roadmap.

For businesses currently relying on centralized providers, evaluating high-volume alternatives for PayPal often highlights the efficiency gains of such sovereign account-to-account rails.

How does the Wero app work?

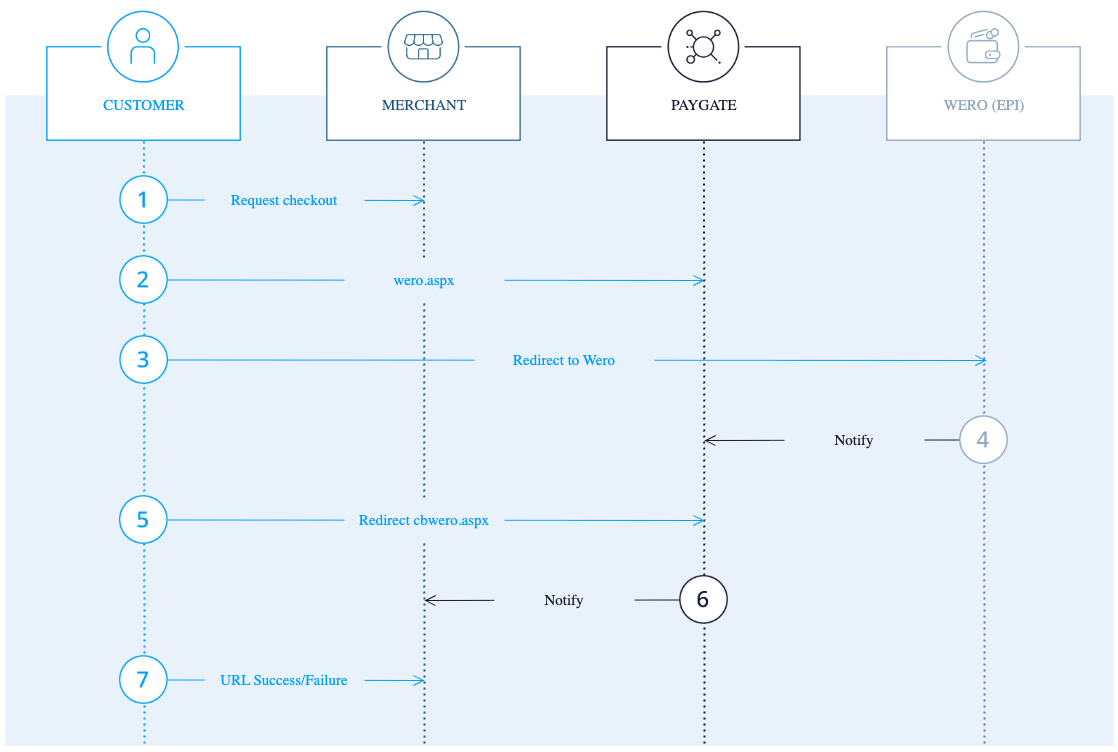

The Wero app facilitates instant payments by utilizing phone numbers or email addresses as unique identifiers, bypassing the need for complex IBAN entries.

Technically, Wero is available both as a standalone application on iOS and Android and as an integrated feature within the mobile apps of member banks. Users create an account by linking their existing bank account, allowing them to send funds directly to a recipient's wallet in real-time. This system is designed to support multiple use cases, starting with peer-to-peer (P2P) transfers and expanding into online checkout and in-store point-of-sale (POS) payments. To maximize security, the app leverages native bank biometrics, which is a core tenet of building a truly unbannable payment architecture.

Wero vs. PayPal vs. Apple Pay: A Comparative Analysis

Wero distinguishes itself from global competitors by functioning as a sovereign European rail rather than an overlay on top of US-based card infrastructure.

While Apple Pay and Google Pay provide a fast, secure user experience through tokenization, they still rely on the underlying American card rails and their associated interchange fees. Wero, by contrast, operates on account-to-account (A2A) rails, moving money directly between European bank accounts. According to G2 comparison data, while PayPal excels in user-friendliness, it often requires an extra login step, whereas A2A settlement happens in seconds without intermediaries.

| Criterion | Wero (EPI) | Visa / Mastercard |

|---|---|---|

| Primary Rail | SEPA Instant (SCT Inst) | Card-based Private Rail |

| Settlement Speed | Real-time (7-10 Seconds) | T+1 to T+3 Days |

| Fees | A2A Direct (Lower Cost) | Interchange / Scheme Fees |

| Data Residency | European Union (GDPR) | Globalized / US-centric |

| Future Tech | AI Agent Ready (API-first) | Human-centric (Physical Card) |

The Geopolitical Imperative: Why Europe Needs Payment Sovereignty

European payment sovereignty is defined as the continent's ability to manage its financial infrastructure and user data independently of external political or economic influence.

The push for the EPI is driven by the decline of cash and the increasing power of non-European digital payment providers. ECB Executive Board member Piero Cipollone warned that 13 euro area countries currently lack any national alternative to international networks.

“As European citizens, we want to avoid a situation where Europe is overly dependent on payment systems that are not in our hands,” Cipollone remarked during a 2026 briefing.

This focus on local control is a primary reason why many firms are now navigating the MiCA regulatory framework and adopting self-hosted payment gateways to ensure long-term resilience.

European alternatives to Visa and Mastercard ‘urgently’ needed, says banking chief

by u/JackRogers3 in europe

Data Residency and GDPR Compliance in EU Payments

A critical component of sovereignty is the requirement that European citizens' payment data remains under the jurisdiction of EU legislation and is managed on the continent.

By processing transactions through an internal European consortium, the EPI adheres strictly to GDPR and data residency rules. This prevents foreign entities from setting rules in foreign boardrooms regarding how European consumer data is analyzed, ensuring that financial privacy is governed by European values. For organizations that handle sensitive user data, moving to non-custodial payment solutions provides an additional layer of privacy and compliance with evolving EU data rules.

The Technical Engine: SCT Inst and Account-to-Account (A2A) Payments

The technical foundation of the EPI is the SEPA Instant Credit Transfer (SCT Inst) scheme, which enables real-time, 24/7 bank-to-bank transactions.

Unlike the legacy toll-bridge model of card networks, Wero uses an account-to-account (A2A) model. As of early 2026, 88% of SEPA participants in the euro area are registered for SCT Inst, with many countries already achieving 100% participation. This architecture moves funds in under 10 seconds, significantly reducing the cost-efficient chain for merchants seeking real-time liquidity.

“A clear blueprint is required so that industry stakeholders can assess the viability of offering EPI functionality,” reports industry analysts at PaymentsJournal

Understanding the Back-end Push and CPACE Standards

The EPI follows a back-end technology push that standardizes domestic card schemes using Common Payment Application Contactless Extensions (CPACE) technical specifications.

This layered development strategy focuses on first migrate, then upgrade. By implementing uniform European standards like CPACE, the EPI ensures that a Wero transaction is technically consistent across borders. This core infrastructure allows banks to build their specific banking apps with advanced security and on-chain risk management features. This is essential for merchants operating in high-risk environments who need robust, standardized technical protocols.

Roadmap to 2027: The Consolidation of National Payment Schemes

The EPI strategy involves the systematic acquisition and integration of successful national payment systems to achieve immediate scale across Europe.

Rather than competing from scratch, the EPI is absorbing national champions to create a single interoperable network. This consolidation is a live market reality that will eventually replace or connect domestic systems into a unified ecosystem covering 13 countries.

“Success in the first core markets is crucial to initiating a broader move to Wero at European level,” says Martina Weimert.

This is especially relevant for businesses reaching new global markets that must adapt to regional e-commerce payment standards.

When will Wero replace iDEAL?

The integration of iDEAL into the Wero framework will begin in 2026, with the goal of fully phasing out the Dutch domestic system by the end of 2027.

This mandatory migration means that Dutch merchants, who currently process 73% of all online purchases via iDEAL, will need to transition their technical integrations to support Wero. Merchants who automate their payment swaps and manage their compliance will be best positioned to handle this large-scale migration.

Which banks are participating in the European Payments Initiative?

The EPI is supported by a coalition of over 16 leading European financial institutions, including several national champions in the banking sector.

Participating entities include:

- France: BNP Paribas, Groupe BPCE (including Banque Populaire and Caisse d'Epargne), Crédit Agricole, Crédit Mutuel (BFCM), La Banque Postale, and Société Générale.

- Germany: Deutsche Bank, DZ Bank, and Sparkassen-Finanzgruppe (DSGV).

- Netherlands: ABN Amro, ING Group, and Rabobank.

- Belgium: Belfius and KBC Bank.

- Spain: BBVA, CaixaBank, and Banco Santander.

- Poland: PKO Bank Polski.

- Finland: OP Financial Group.

- Acquirers/Processors: Nexi and Worldline.

Spanish Banking Consortium (Collective Shareholders)

- ABANCA, Banco Cooperativo Español, Grupo Cooperativo Cajamar, Caja de Ingenieros, LABORAL Kutxa, Cecabank, Eurocaja Rural, Grupo Bankinter, Ibercaja, Kutxabank, Liberbank, and Unicaja Banco.

Participating Consumer Member Banks by Market

- Belgium: Argenta, Bank van Breda, Beobank, Crelan, and vdk bank.

- Germany: BBBank, GLS Bank, Postbank, and PSD Bank.

- France: CIC, Crédit Mutuel Arkéa, Fortuneo, and Hello bank!.

- Netherlands: bunq, KNAB (BAWAG AG), and Mollie.

- Luxembourg: Banque Internationale à Luxembourg (BIL), Banque Raiffeisen, BCEE Spuerkeess, BGL BNP Paribas, and Post Luxembourg.

Digital and Neo-Banks

- Revolut.

- N26.

- bunq.

Merchant Implementation: Transitioning to the New Standard

For merchants, Wero offers a more cost-efficient chain and faster settlement, but it requires significant updates to internal treasury management systems.

The transition to real-time liquidity management is a fundamental shift from traditional multi-day card settlement cycles. Under new EU regulations, merchants will likely be required to accept digital euros by 2029, making current Wero adoption a logical first step.

“Merchants will benefit from a simplified onboarding process through a solution developed by and for Europeans,” notes an EPI media update.

This trend mirrors the shift toward stablecoin payments which unbanks markets via direct account access.

Integration Challenges for US Businesses Operating in Europe

US businesses with a European presence must prepare to re-integrate their payment gateways as domestic methods like iDEAL are retired in favor of Wero.

As the Eurozone moves toward a unified standard, US merchants who previously optimized checkouts for national schemes must now align with the pan-European method. This shift may impact tourist spending patterns, making it vital to explore unbannable payment solutions and strategies for high-risk merchant survival in a changing regulatory landscape.

Future Trends: Agentic Commerce and the AI Transition

The API-first A2A model of the EPI is inherently more compatible with the rise of Agentic Commerce, where AI agents autonomously handle transactions for users.

By 2030, global agentic commerce volume is projected to reach $5 trillion. Traditional card networks rely on human-centric authentication, which can be difficult for an AI agent to navigate. By contrast, protocols like X402 or the Model Context Protocol (MCP) allow for secure, machine-readable internet-native payments.

“Agentic will be a paradigm shift for e-commerce,” says Morgan Stanley internet researcher Nathan Feather

Preparing for this future requires businesses to integrate autonomous AI agent payment capabilities today.

The Intersection of EPI and Web3 Payments (PayFi)

While current plans are fiat-focused, the broader industry is looking toward blockchain-based rails, known as PayFi, to combine global reach with instant settlement.

Blockchain networks provide similar real-time movement benefits to SCT Inst but on a global scale. If the EPI aims to be truly future-proof, its roadmap may eventually need to address Tether (USDT) and digital assets. Innovators are already using TRON (TRX) to slash fees and increase settlement speed while maintaining blockchain-grade security and transparency.

Beyond Centralized Rails: PayRam and the Future of Permissionless Commerce

While the European Payments Initiative successfully reclaims sovereignty from global giants, it still operates within a centralized bank-consortium model where intermediaries maintain control over the flow of funds. A parallel movement is emerging that moves entirely away from centralized rails toward permissionless commerce. This paradigm shift, led by processors like PayRam, focuses on the original principles of blockchain-based finance: privacy, self-custody, and trustless settlement.

By allowing merchants to deploy their own self-hosted payment nodes, businesses can achieve end-to-end ownership of their payments stack. This effectively addresses common systemic risks such as account freezes, withheld balances, and transaction blacklisting that persist even in modern domestic systems.

The goal is to build a decentralized PayFi layer where every merchant or creator can host and own their own infrastructure, ensuring that the future of money moves across the internet as freely as the information that precedes it. - Siddharth Menon, Founder - PayRam

What companies are involved in the European Payments Initiative?

The EPI is a consortium of 16 major shareholders including banks like BNP Paribas, Deutsche Bank, ING, Santander, and Société Générale, along with payment processors such as Nexi and Worldline.

How does the EPI compare with other global payment networks?

Unlike Visa or Mastercard, which are American-governed card networks, the EPI is a European-owned account-to-account (A2A) system that settles funds in real-time without the need for card overlays.

What is the new unified mobile payment system for Europe?

The brand for the EPI's unified payment system is Wero, a digital wallet that allows users to send and receive money instantly using phone numbers or email addresses across participating EU countries.

How to create an account on the Wero app?

Users can typically activate Wero directly through their existing participating European bank app or by downloading the standalone Wero app and linking their bank account via secure biometric authentication.

When will Wero replace iDEAL?

The migration of iDEAL to Wero is scheduled to begin in 2026, with a complete phase-out of the iDEAL brand and technical system by the end of 2027.

Which banks support the EPI?

Major supporters include the Sparkassen and Volksbanken in Germany, the big five banks in France, and several major institutions in Belgium and the Netherlands, with expansion plans for Luxembourg and Italy.

How will the digital wallet impact tourist spending?

For US travelers, Wero may become the preferred method for merchants in certain Eurozone regions. Tourists may need to set up digital wallet accounts or ensure their cards are compatible with Wero-accepting terminals.

Can US businesses integrate the new payment gateway?

Yes, US businesses operating in the EU can integrate Wero to offer local consumers a familiar checkout experience, though they must adapt to real-time liquidity management standards.

What is the daily transaction limit for Wero?

Transaction limits are set by individual member banks, but the system is engineered to handle both small P2P transfers and high-value business invoice settlements through the SCT Inst rail.

How secure is Wero for data privacy?

Wero is governed by EU-based data residency rules and is fully GDPR-compliant, ensuring transaction data is not sold or analyzed by non-European third parties in foreign boardrooms.

Conclusion: Embracing Europe’s Sovereign Financial Future

The European Payments Initiative represents the most credible challenge to the transatlantic duopoly of Visa and Mastercard in decades. By consolidating national champions into the Wero standard and leveraging the technical efficiency of account-to-account payments, the EPI is not just building a wallet—it is reclaiming the continent's financial destiny. For businesses, the message is clear: the ERA of the transatlantic duopoly is facing a live market shift. Monitoring the 2026-2027 roadmap for Wero and the consolidation of systems like iDEAL is no longer optional, it is a critical requirement for anyone operating within the European market.

Ready to modernize your payment infrastructure for the next generation of global commerce?

Contact Payram today to explore how our cross-border solutions can future-proof your business.