February 12, 2026

Ask GPT about this BlogSWIFT vs. Stablecoins: The Future of Global Business Settlement and Sovereignty

For decades, the standard for moving money across borders has been the SWIFT network, a system that revolutionized the 1970s by replacing the manual errors of Telex with standardized digital messaging. However, as we enter 2026, a fundamental shift is occurring. Businesses are moving beyond legacy messaging toward internet-native finality, a paradigm where value and information move as one. The choice between SWIFT and stablecoins is no longer just about choosing a faster rail. It is a strategic decision about who owns your payment infrastructure and how you maintain sovereignty over your revenue by following a comprehensive guide to cryptocurrency payments.

The Great Settlement Divide: SWIFT Messaging vs. Blockchain Finality

Stablecoins provide atomic settlement where value and information move together, while SWIFT acts as a messaging-only layer for legacy bank reconciliation.

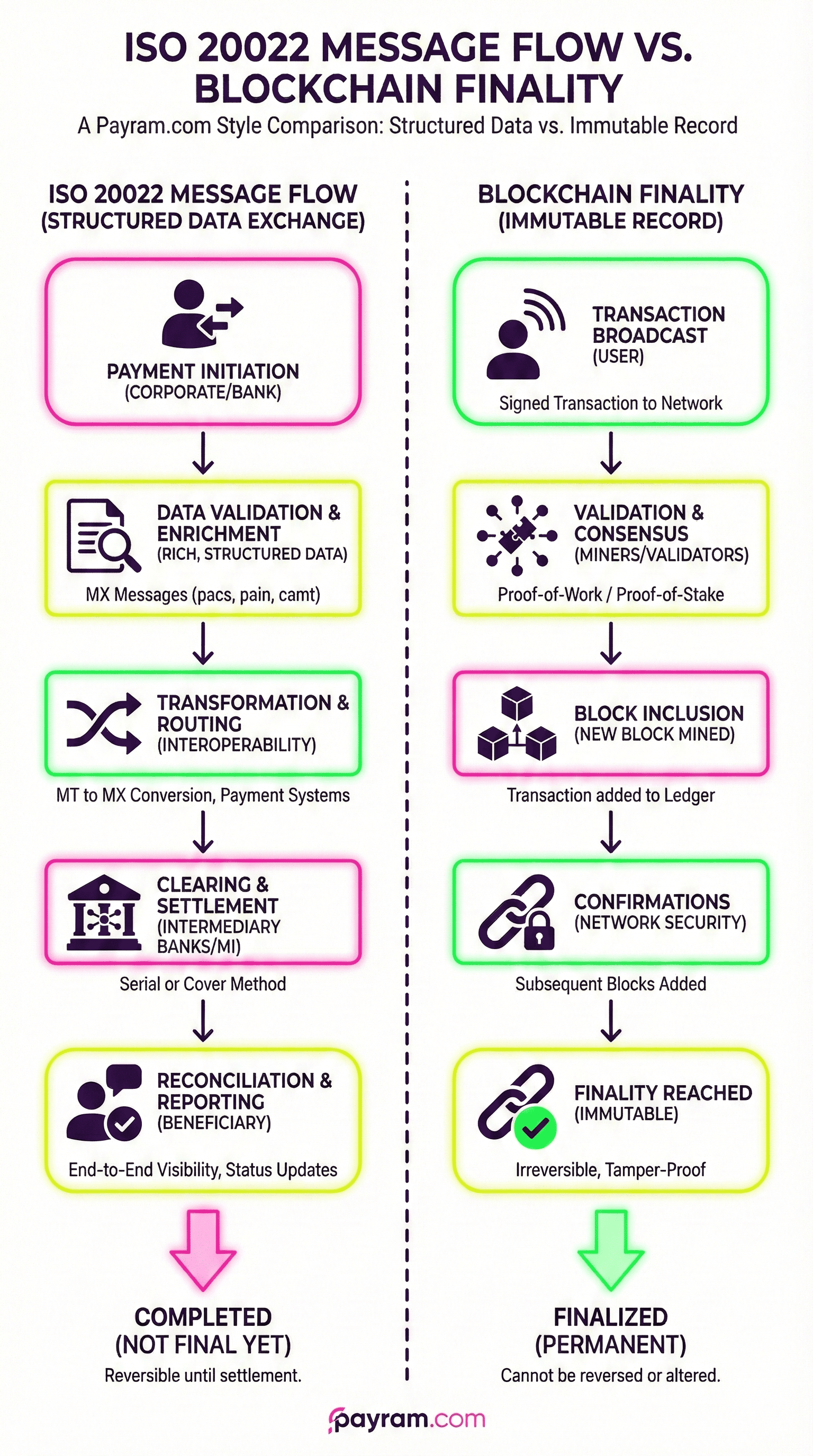

SWIFT, the Society for Worldwide Interbank Financial Telecommunication, does not actually move money. Instead, it moves instructions about money. When a bank sends a SWIFT message, it is essentially sending an IOU that must be reconciled across multiple intermediaries before the funds are considered settled. Stablecoins utilize blockchain technology to achieve atomic settlement. In this model, the transfer of the asset and the finality of the transaction happen simultaneously on a shared ledger, removing the need for a separate reconciliation process. To understand the full scope of this shift, you can explore PayRam and how it facilitates direct settlement.

Stablecoins currently account for $30 billion in daily transaction volume, rapidly approaching the volume of legacy card networks.

“Swift for stablecoins” isn't just about creating faster, cheaper, and transparent cross-border transactions, but building a foundation for the next generation of programmable money, real-world finance, and global innovation. - Michael Shaulov, CEO of Fireblocks

You can read more about this in our onchain payments guide to see how it applies to stablecoin business use cases.

What are the main differences between international bank transfers and stablecoin transactions?

International bank transfers rely on a chain of intermediaries and manual reconciliation, while stablecoin transactions utilize direct peer-to-peer settlement on a 24/7 blockchain ledger.

| Criterion | Legacy SWIFT Network | Stablecoin Rail (PayRam) |

|---|---|---|

| Settlement Speed | 1 to 5 Business Days | Seconds to Minutes |

| Core Model | Messaging-only (Requires Banks) | Atomic Settlement (Value + Info) |

| Processing Fees | $10–$50 Wire Fees + FX Spreads | 0% processing fees with self-hosted stack |

| Infrastructure Control | Custodial (Banks can freeze funds) | Non-Custodial (Your Keys, Your Revenue) |

| Transparency | Private (Opaque intermediaries) | Public Ledger (Real-time audit) |

| Availability | Banking Hours (Mon–Fri) | 24/7/365 Global Access |

How atomic settlement eliminates multi-day financial plumbing delays

Atomic settlement collapses the instruction and payment layers into a single event, allowing businesses to access working capital in seconds rather than days.

In traditional finance, funds are often trapped in the financial plumbing of intermediary banks, creating liquidity gaps that can last for days. By using blockchains like Solana or Polygon, which offer near-instant finality, businesses can receive a payment and immediately redeploy those funds for payroll or inventory. This shift from legacy messaging to blockchain finality represents a fundamental rewiring of the global financial stack. For more on the technical specifications, see the distributed ledgers smart contracts business standards.

Deconstructing the Legacy Rail: Why SWIFT Transfers Take 1–5 Days

The SWIFT network’s 1 to 5 day delay is caused by the sequential nature of correspondent banking and the manual reconciliation of nostro and vostro accounts.

The primary reason for SWIFT’s lag is its reliance on the correspondent banking model. If Bank A in New York does not have a direct relationship with Bank B in Singapore, the payment must hop through one or more intermediary banks. Each intermediary performs its own compliance checks and adds its own processing time. If your business has ever experienced the frustration where Stripe closed your account, you know how critical it is to find a high-risk merchant survival guide that bypasses these delays.

Over 1.4 billion people remain unbanked globally, a gap that legacy SWIFT architecture is structurally unable to close due to its reliance on institutional bank accounts.

Traditional bank transfers are constrained by domestic payment systems, layered infrastructure, and settlement delays, whereas stablecoins go peer to peer and can be anywhere in the world. - Tom Rhodes, Chief Legal Officer of Agant

Why does a SWIFT transfer take so long?

SWIFT transfers are slowed by manual compliance screenings, time zone mismatches, and the limited operating hours of local central bank clearing systems.

The friction points in a SWIFT transfer include:

- Intermediary Screening: Each bank in the chain must verify the transaction against local AML and KYC regulations.

- Time Zone Mismatches: A transfer initiated on a Friday afternoon in New York may not be processed until Monday morning in Tokyo.

- Batch Processing: Banks often process payments in windows rather than in real-time, leading to further delays if a window is missed. These issues make PayPal alternatives for high-volume transactions an essential consideration.

The role of correspondent banking and Nostro/Vostro accounts

Correspondent banking relies on a network of ledger entries in nostro and vostro accounts that must be manually aligned across different time zones.

Traditional cross-border settlement is essentially a manual ledger exercise. Banks maintain accounts with one another: a nostro (our money with you) and a vostro (your money with us). This reconciliation is tied to regional high-value clearing systems like Fedwire (USD) or T2 (EUR), which operate only during specific business hours, making 24/7 settlement impossible.

The ISO 20022 (MX) migration and its 2025 deadline

The global financial system is currently migrating to the ISO 20022 standard to improve the quality of payment data, with a critical implementation deadline in late 2025.

To address the high rate of manual interventions caused by unstructured data, SWIFT is migrating from legacy MT messages to the XML-based ISO 20022 (MX) standard. This migration provides clear, labeled fields that allow for better automated screening. The deadline for this coexistence period is November 22, 2025, after which all messages must use the new MX format.

The Stablecoin Taxonomy: Navigating Fiat-Backed, Crypto-Collateralized, and Algorithmic Tokens

Business treasuries should prioritize fiat-backed stablecoins like USDC and USDT due to their transparency and 1:1 reserve backing compared to more volatile crypto-collateralized models.

For corporate use, not all stablecoins are created equal. Digital assets represent different technical approaches to maintaining price stability. You can dive deeper into USDT and view a direct comparison of USDC to decide which fits your treasury.

Combined, Tether (USDT) and Circle (USDC) make up approximately 85% of the fiat-pegged stablecoin market, providing the majority of the world's on-chain liquidity.

Cross-border payments that are right now going through stable coins, which is less than one percent, will head to about 30 to 40 percent in the next three years. - Anand Bindumadhavan of Triple-A

Learn how to choose the right crypto rail to optimize your transaction strategy.

Which stablecoins are safest for business cross-border payments?

Fiat-backed stablecoins like USDC and USDT are generally considered the safest for commerce because they are backed 1:1 by highly liquid reserves like cash and US Treasuries.

Fiat-collateralized tokens account for the vast majority of the total stablecoin market share. These assets offer the predictability required for corporate accounting, as they act as digital representations of the dollar that live on the blockchain.

Comparing Tether (USDT) and Circle (USDC) for Corporate Treasury

Tether (USDT) and Circle (USDC) are the dominant stablecoin options, differing primarily in their regulatory jurisdiction and the specific blockchain networks they prioritize.

- Tether (USDT): The oldest and largest stablecoin, frequently used on the Tron and Ethereum networks. It is widely used for international remittances and in emerging markets.

- Circle (USDC): The largest US-onshore stablecoin, often preferred by regulated institutions due to its transparency and reserve attestations. It is a primary asset on Ethereum and Solana.

Infrastructure Sovereignty: The Shift from Custodial to Self-Hosted Gateways

Owning your payment infrastructure through self-hosted gateways provides absolute censorship resistance that custodial providers cannot offer.

The real evolution of global settlement isn't just about using stablecoins. It is about how you accept them. Moving from custodial services to self-hosted software is a pivot toward true financial sovereignty. Before choosing a provider, read about custodial vs non-custodial crypto payment gateways to understand the risks.

Merchants in high-risk categories face chargeback rates as high as 4.79% in education and 4.68% in travel, leading to frequent account terminations by traditional processors.

AI and stablecoins are rewriting the rules, payments companies that aren't AI-first may not survive the next three years. - Arik Shtilman, Founder and CEO of Rapyd

Discover what is self-hosting and why it is the ultimate guide to digital sovereignty.

The Custodial Trap: Why centralized crypto processors replicate bank risk

Centralized crypto gateways act as intermediaries that can freeze accounts and withhold funds, mimicking the same platform risks found in traditional banking.

Custodial gateways act as trusted third parties. While they process stablecoins, they still maintain control over your revenue and require mandatory business verifications. For a merchant, this means you are once again a guest on their platform, subject to their arbitrary rules. This is why the unbannable gateway is the only true defense for modern businesses.

Architecture of an Unbannable Gateway: xPubs and No Keys on Server

Self-hosted gateways like PayRam use xPub architecture to derivation unique deposit addresses while keeping private spending keys securely offline.

A sovereign gateway uses an Extended Public Key (xPub) architecture. This allows the server to derivation fresh, unique deposit addresses for every customer order without ever possessing the private keys required to spend the funds. To learn more about how this works, read our guide on seed phrases & HD wallets. The merchant keeps their private keys in offline cold storage, ensuring that the funds move peer-to-peer directly into their possession.

Economic Optimization: Reclaiming Gross Revenue Through Zero-Fee Settlement

Switching to stablecoin settlement through self-hosted software allows businesses to recapture percentage-based fees and redirect them back into profit margins.

The economic argument for stablecoins is undeniable. Traditional processors and SWIFT transfers involve a series of rent-seeking fees that siphoned off a percentage of every sale. You can analyze how these fees are structured in our report on Visa Mastercard swipe fee settlement.

A merchant processing $1 million in monthly revenue can recapture approximately $120,000 per year in profit by moving from a 2.9% fee structure to the zero-fee settlement model.

when you've been using stablecoins to transfer value across the world and then all of a sudden you're on to legacy systems, you realise the efficiencies. - Andrew MacKenzie, co-founder of Agant

Review the 2025 E-commerce revolution to see how self-hosted payments slash fees.

How do fees compare between traditional wire transfers and stablecoin payments?

Stablecoin payments through self-hosted gateways eliminate percentage-based fees, replacing them with flat infrastructure costs and minimal network gas fees.

For a business processing significant monthly revenue, the difference is stark. Traditional gateways take a massive cut of every transaction. With a self-hosted gateway, businesses recapture that capital, paying only flat infrastructure costs for their own private server.

The Agentic Economy: Enabling AI Agents with x402 and HTTP Native Payments

The x402 protocol enables autonomous AI agents to conduct real-time machine-to-machine payments without human intervention, unlocking a new era of commerce.

The shift to stablecoins is the foundation for Agentic Commerce, where AI agents autonomously search, negotiate, and pay for services. This is explained in our guide to what is agentic commerce. This requires a new set of standards that traditional banking rails simply cannot support.

Agentic AI is projected to drive up to $17.5 trillion in global commerce by 2030, representing a massive shift in how the internet functions.

if the agent economy is real, the payment layer won't be optional, it will be foundational. - Consu Valdivia of Shinkai

Read about x402 protocol and how it powers OpenClaw & Agentic Commerce.

x402 micropayments in practice: AI agents paying for API calls on Base

by u/Klutzy_Car1425 in ethdev

What is the x402 protocol and how does it power AI agents?

x402 activates the HTTP 402 Payment Required status code to create an internet-native handshake for programmatic machine payments.

The x402 protocol works as follows: An AI agent requests a resource, the server responds with an HTTP 402 error containing a price, the agent's wallet signs a signature, and the transaction settles on-chain in seconds.

From subscriptions to micropayments: The machine-to-machine revolution

Stablecoin rails enable granular, per-use pricing models that are economically impossible on credit card networks due to high fixed fees.

Traditional rails are too expensive for micropayments. By using x402 on low-cost networks like Base or Polygon, AI agents can pay exactly for what they consume, shifting the internet from subscriptions to economic workflows.

PayFi and Treasury 2.0: Monetizing the Float with Yield-Bearing Assets

PayFi transforms traditional "float" from a bank-held asset into a yield-generating engine for the business.

Beyond simple payments, the emergence of PayFi (Payment Finance) allows businesses to monetize the time their money is in transit. Our PayFi explainer details this quiet upgrade to the global financial system.

McKinsey & Co. projects that stablecoin daily volume will grow from $30 billion to $250 billion within the next 36 months as treasury adoption increases.

Chris Xie, CEO of 4Alpha Group - Introduced a quant-driven liquidity model, stating it proposes “payment + yield” as a sustainable architecture for institutions seeking to monetize float while remaining compliant.

Use our CFO guide to stablecoin yield to compare PayFi vs DeFi.

Beyond payments: Generating yield on working capital in real-time

Corporate treasurers can now earn immediate returns on their stablecoin balances by utilizing tokenized money-market funds and DeFi lending protocols.

In the SWIFT model, banks earn interest on the float while your money is stuck in transit. In the PayFi model, treasurers can instantly swap stablecoins for yield-bearing assets or tokenized US Treasuries, ensuring their working capital is always productive.

Liquidity management without bank cut-off times

Stablecoins offer treasurers 24/7 access to intraday liquidity, eliminating the constraints of banking holidays and batch processing windows.

This always-on access allows for intraday treasury sweeps, pooling cash from global subsidiaries into a single stablecoin treasury at any time, significantly reducing the need for large cash buffers.

Navigating the Regulatory Frontier: MiCA, the GENIUS Act, and Beyond

Maturing global frameworks like MiCA and the GENIUS Act are providing the legal certainty necessary for institutional stablecoin adoption.

Stablecoin regulation is rapidly moving from theory to practice. Businesses must understand EU’s MiCA (Markets in Crypto-Assets) and The GENIUS Act to remain compliant.

The European Union’s MiCA regulation is the first comprehensive framework in the world specifically designed to mandate strict reserve management for stablecoin issuers.

Lucas Yang of Cobo believes that stablecoins are no longer just digital IOUs—they're evolving into mission-critical infrastructure for global payments.

Reference our guides on on-chain risk management and FATF (Travel Rule).

What are the regulatory considerations for using stablecoins?

Global stablecoin adoption is increasingly governed by region-specific frameworks that mandate strict reserve management and transparency.

Governments in the EU, the US, and Asia are introducing licensing regimes for fiat-backed stablecoin issuers to facilitate cross-border trade while protecting systemic stability.

Compliance by design: Embedding governance into smart contracts

Programmable stablecoins allow compliance and sanctions checks to be embedded directly into the transaction protocol rather than being handled as a separate, manual layer.

Unlike SWIFT, where compliance is a manual hurdle, stablecoins allow for built-in governance. Smart contracts can autonomously enforce rules, such as blacklisting sanctioned addresses or setting spending limits.

Strategic Implementation: Building Your Sovereign Financial Stack

Transitioning to a sovereign financial stack is a three-step process involving infrastructure deployment, machine-economy readiness, and fiat-bridging integration.

Building an unbannable payment stack is a strategic pivot. You can find out more by reading about self-hosted crypto payment gateways and how they build your crypto fortress.

Businesses can go live with a self-hosted gateway in under 10 minutes using modern GUI-based installation methods.

Michael Zhao, CEO of Klickl, describes reimagining open banking for Web3 as a native account system supporting institutional fund flows, asset conversion, and multi-currency settlement.

We provide the best crypto payment gateway for casinos and high-stakes marketplaces. Learn about circle's superhighway in our guide on what is Arc blockchain.

Steps to deploy a non-custodial gateway in under 10 minutes

Deploying a sovereign gateway requires setting up a private server, importing an xPub, and configuring automated fund management tools.

- Deploy the Software: Host your own instance on a VPS via Docker.

- Import Your xPub: Mathematically link your offline wallet to derive unique payment addresses.

- Configure SmartSweep: Automate the orchestration of funds from thousands of addresses into your main treasury wallet.

The competition between SWIFT and stablecoins is ultimately a competition between a legacy network of intermediaries and a modern protocol of sovereign actors. While SWIFT remains a vital rail for interbank trade, stablecoins are the superior default for the digital-native enterprise. By combining the speed of atomic settlement with the sovereignty of self-hosted architecture, businesses can finally achieve financial independence.

SWIFT vs Stablecoins: Frequently Asked Questions

How long does a SWIFT transfer take compared to a stablecoin payment?

A typical SWIFT transfer takes between 1 and 5 business days because it must pass through multiple intermediary banks and regional clearing systems. In contrast, a stablecoin payment settles on-chain in seconds or minutes, offering near-instant finality 24/7.

Why is a self-hosted gateway considered unbannable?

A self-hosted gateway is unbannable because the software runs on your own server infrastructure rather than on a third-party platform. Since you maintain 100% custody of your private keys and funds, no central authority or payment processor can freeze your account or terminate your service.

What is an xPub and why is it important for payment privacy?

An xPub, or Extended Public Key, allows a payment gateway to generate an infinite number of fresh deposit addresses for your customers without ever needing your private spending keys. This ensures that your actual funds remain securely offline while the server tracks incoming payments transparently.

Are there hidden fees when using SWIFT for international transfers?

Yes, SWIFT transfers often include stacked fees such as intermediary bank charges, wire transfer costs ranging from $10 to $50, and significant markups on foreign exchange spreads. These costs are often deducted from the principal amount before it reaches the recipient.

How does the x402 protocol facilitate AI agent payments?

The x402 protocol uses the standard HTTP 402 "Payment Required" status code to create a machine-native handshake. When an AI agent requests a resource, the server provides a price and wallet address, and the agent pays instantly with stablecoins to unlock access without human intervention.

What is the difference between PayFi and traditional DeFi?

PayFi focuses on the intersection of payment processing and finance, specifically looking at how to monetize the float and generate yield on working capital during the payment cycle. Traditional DeFi focuses more on decentralized trading, lending, and borrowing of crypto assets.

Is using stablecoins compliant with regulations like MiCA?

Yes, the EU's MiCA regulation provides a clear legal framework for the issuance and use of stablecoins. By using fiat-backed stablecoins from regulated issuers, businesses can conduct cross-border transactions while meeting high standards for transparency and reserve management.

Can high-risk industries use stablecoins to avoid chargebacks?

Stablecoin transactions on the blockchain are final and irreversible. This completely eliminates the risk of fraudulent chargebacks, which can cost high-risk merchants up to 18% of their annual profit in traditional payment systems.

Which is better for corporate treasury: USDT or USDC?

Both USDT and USDC are highly liquid digital dollars. USDC is often preferred by US-regulated institutions due to its onshore transparency, while USDT remains the dominant global asset for high-volume cross-border trade and emerging market remittances.

What does the SWIFT gpi tracker do?

The SWIFT GPI (Global Payments Innovation) tracker provides real-time visibility into the status of a bank wire. It allows finance teams to see where a payment is in the chain and what fees have been taken, though it still operates within legacy banking windows.

Ready to reclaim your financial sovereignty?

Deploy your own self-hosted payment gateway in minutes and start processing zero-fee stablecoin payments today. Visit PayRam to get started.